Ethena’s Yield-Dollar Odyssey: From Genesis to Convergence

USDe could become what Eurodollars were in the 20th century: a parallel monetary system operated outside traditional banking, yet integral to it

Before we dive in, a quick word to the two audiences reading side-by-side. To the crypto-native crowd, consider this a deep-dive refresher; to my friends in traditional finance, think of it as a front-row view of how innovation happens when financial primitives are rebuilt from scratch. Ethena’s journey is a window into DeFi’s boldest experiment yet: creating a permissionless, yield-bearing, dollar-denominated asset that works as a savings instrument, collateral and can be used for retail or cross-border payments — all at once, for anyone, anywhere with a smartphone. DeFi’s magic lies in this composability, in its ability to stitch together global liquidity without asking for permission. The trade-off, of course, is a new risk stack: smart-contract exploits, oracle bugs, regulatory whiplash and more. Yet the builders keep building, because if DeFi could crack a better form of money — transparent, programmable, and open — it won’t just be crypto’s win. It’ll be finance’s evolution.

1. Genesis – A New Vision for a Dollar with Yield

In March 2023, Arthur Hayes published “Dust on Crust,” envisioning crypto’s “largest opportunity”: a synthetic dollar backed by crypto and its peg maintained by derivatives. The idea was simple yet profound – “the most important financial instrument on earth to save and preserve wealth is simply a dollar with a yield”. This thesis resonated deeply in a post-UST world: demand for a yield-bearing, bankless dollar was orders of magnitude larger than crypto’s entire market, including Bitcoin. A small team led by Guy Young (Ethena’s founder) took up Hayes’ challenge. By July 2023, Ethena Labs was born to build “internet money” – a fully-backed, crypto-native stablecoin with an objective to force convergence of capital and interest rates across DeFi, CeFi and TradFi.

Launch on Ethereum Mainnet: Ethena chose Ethereum as its genesis chain for the deepest liquidity and DeFi composability. The protocol’s core stablecoin, USDe, launched on the mainnet on February 19, 2024. Being Ethereum-native also lent credibility; in the wake of scrutiny on bank-backed stablecoins, Ethena positioned USDe as a censorship-resistant alternative. Ethena’s USDe is “not the same as a fiat stablecoin like USDC or USDT” – there are no bank deposits behind it. Instead, it’s fully crypto-backed and delta-hedged on derivatives markets, with fundamentally different risk dynamics.

USDe maintains its stability using a delta-neutral strategy, meaning it balances long and short exposures so that the net position has near-zero sensitivity to market direction. For example, when a user mints USDe, Ethena takes that collateral (typically ETH or BTC) and stakes it to earn staking rewards. But because staking exposes the protocol to price movements of that asset, Ethena simultaneously opens an equivalent short position via perpetual futures on platforms like Binance or Bybit.

So if the price of ETH goes up, the value of the staked ETH rises, but the short position loses an equal amount, keeping the net exposure flat. Similarly, if ETH prices decline, the loss on the staked ETH is offset by a gain on the short. This hedged position ensures that the protocol doesn’t take a directional bet on crypto prices and allows USDe to remain stable regardless of market volatility.

The yields that sUSDe (it’s the staked version of USDe, making it a yield-bearing ERC-4626 token) or iUSDe (an institutional-grade counterpart to sUSDe, wrapped with transfer restrictions and KYC/whitelisting via Securitize—delivering the same yield engine but only to accredited, compliance-approved participants) holders earn come from two sources: the staking rewards on the long ETH position and the funding rate received from holding the short perps position, especially in bullish markets where perps trade at a premium. This combination is what powers the yield engine behind USDe without compromising its peg.

When users stake USDe in Ethena’s app, they receive sUSDe, which automatically accrues yield. Importantly, sUSDe’s balance doesn’t increase; instead, each sUSDe grows in value vs USDe, redeemable for more USDe over time as yield compounds. This design (similar to Lido’s stETH or Rocket’s rETH) means sUSDe always stays liquid and dollar-pegged (roughly), while embodying a growing claim on the underlying collateral yields. In essence, USDe is a stablecoin for payments and DeFi, and sUSDe is a stable, on-chain savings account which is also composable, offering what banks couldn’t: uncensorable dollars with native yield.

In ERC-4626 terms, each sUSDe token represents a share in the vault, whose exchange rate is defined as:

exchangeRate = totalAssets() / totalSupply()where:

totalAssets()is the amount of USDe the vault currently holds (including all accrued yield), andtotalSupply()is the number of sUSDe shares outstanding.

Simple Math Example

At deposit (t=0):

You deposit 1,000 USDe into the vault.

Suppose the vault is empty before you, so

totalAssets = 0,totalSupply = 0.By convention (or initial parameter), you receive 1,000 sUSDe, and now

totalAssets = 1,000

totalSupply = 1,000

⇒ exchangeRate = 1,000 / 1,000 = 1.0So 1 sUSDe = 1 USDe.

After yield accrues:

The vault’s shorting and staking generate 50 USDe in profit, so

totalAssets = 1,050

totalSupply = 1,000

⇒ exchangeRate = 1,050 / 1,000 = 1.05Now 1 sUSDe = 1.05 USDe.

Redemption:

If you redeem your 1,000 sUSDe, you get

1,000 shares × (1,050 assets / 1,000 shares) = 1,050 USDeYour USDe balance has grown by 5% thanks to the vault’s yield.

Whenever new deposits or withdrawals occur, totalAssets and totalSupply change, but the same formula always ensures that each sUSDe share is redeemable for the correct pro-rata amount of USDe, including all the yield earned since minting.

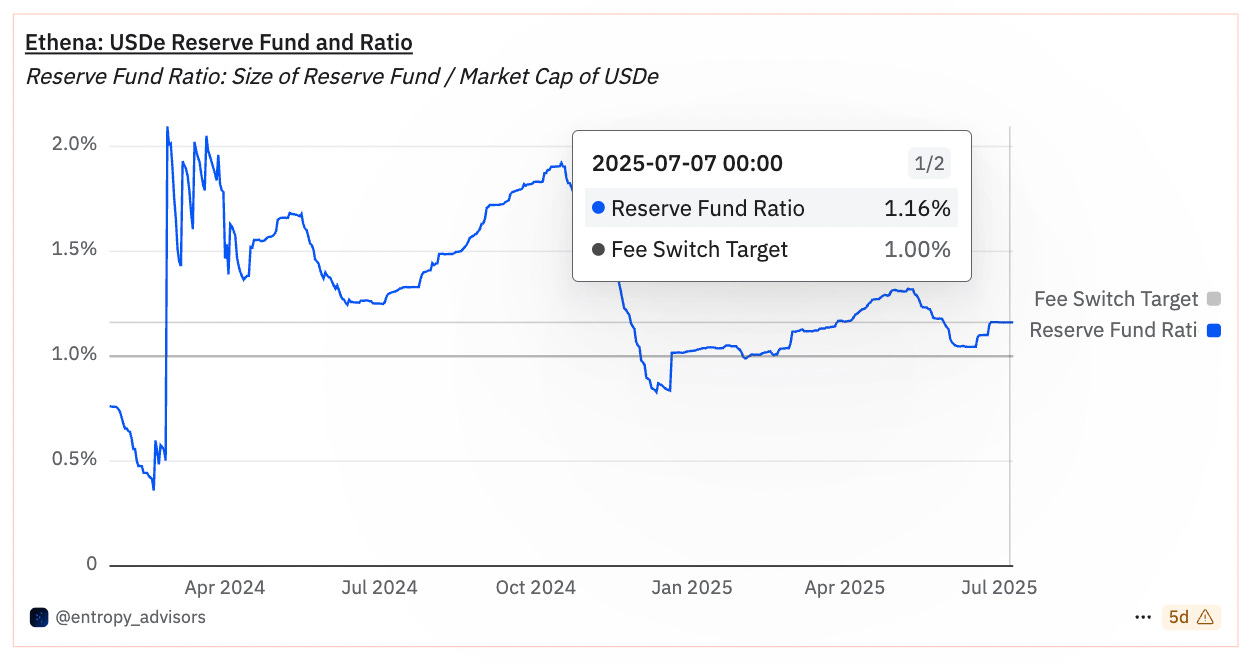

Ethena ring-fences the peg with a “Reserve Fund”, an on-chain insurance pot, by diverting a slice of every funding-rate payout and staking reward into it until the reserve equals roughly 1% of total USDe TVL. That 1% threshold (≈ $50M on a $5B supply) is calibrated as a statistically sufficient buffer to absorb a multi-day stretch of negative funding or surge in withdrawals. The protocol’s “fee-switch” logic is simple: when the reserve exceeds the 1% target, the vast majority of new yield flows straight to sUSDe holders; if the reserve drops below target—say, after a sharp market move—Ethena automatically “skims” a larger share of incoming yield (and, if needed, part of redemption fees) until the reserve is topped back up. In effect, users trade a tiny slice of upside during good times for a robust shock absorber during bad times, aligning with Ethena’s goal of combining high on-chain yield with bank-like loss protection.

Initial Collateral Mix – ETH + stETH: The original blueprint (April 2023) envisioned using ETH as the primary spot collateral, hedged with short ETH futures, effectively creating a stable-value dollar from volatile ETH. Ethena’s team saw a chance to “improve on Hayes’ idea” by incorporating staked ETH (stETH) as collateral. This twist was key: stETH earned ~6–7% APR in 2023, providing a natural yield to buffer any negative funding rates. Historically, perp funding on major exchanges averaged ~8% annualised. Thus, with stETH yielding ~6–7%, Ethena’s dollar could weather funding rates turning somewhat negative without dipping into reserves, a crucial resilience mechanism. In theory, this was “the ideal foundation”: long stETH + short perps, a delta-neutral structure where staking yield plus perp funding creates the yield for sUSDe. This fully on-chain, fiat-free design promised a decentralised stablecoin free from bank runs or blacklists.

Why ETH and stETH? ETH was a logical base collateral given its ubiquity and deep perp markets. stETH (Lido’s liquid staked ETH) added yield and aligns with crypto ethos (securing Ethereum itself). Notably, Hayes’ original vision centred on BTC collateral; Ethena initially explored BTC too, but Ethereum’s staking yield made ETH/stETH more compelling at the start. Risk trade-offs: However, by the time of launch, stETH yields had fallen to ~3% (as ETH staking participation soared post-Merge). This undermined stETH’s appeal: a 3% yield hardly beat U.S. T-bills (~5% at the time), and stETH carried added liquidity and depeg risks (it’s a derivative of ETH with withdrawal queues and occasional market discounts). The team recognised that “holding a less liquid derivative as a significant portion of USDe backing became less appealing, particularly when short-term T-bills were earning 5%+”. Thus, Ethena leaned more on plain ETH at launch, using stETH more sparingly despite its yield.

The delta-neutral strategy’s stability was achieved by continuously rebalancing hedges. This design was validated in practice: during USDe’s first large market stress test (April 2024), ~$100M USDe was redeemed amid a 15% one-day drop in global perpetual open interest (one of the largest OI flushes in a year). USDe’s market price barely wavered, staying within 20 basis points of $1 throughout that sell-off, showcasing Ethena’s robust liquidity management. This episode prompted Ethena to institutionalise a policy of maintaining ample liquid reserves to handle mass redemptions at all times.

The Shard Campaign – Bootstrapping to $1B: Upon launch, Ethena opened with a bang: a Shard Campaign incentivised early adoption, aiming to reach $1B USDe supply within 3 months. The results blew past expectations as USDe hit $1B TVL by March 2024 after launching in November 2023. Soon, USDe emerged as the fastest-growing stablecoin, reaching $2B in TVL by April and $3B in June, achieving those milestones faster than any prior stablecoin.

Behind this explosive growth were two key factors: yield and trust. Ethena was able to offer an attractive APY (~20–30% at launch). Simultaneously, its fully-backed design and big-name backers, including Arthur Hayes himself, lent credibility. In total, Ethena raised a total of $136.5 million across multiple disclosed rounds. Ethena diverted 10%-15% of every fundraise into the Reserve Fund, ensuring the buffer scales with TVL growth and insulating sUSDe holders from hedging or custody shocks. This war chest supported liquidity and reserve buffers from the start, differentiating Ethena from Ponzi-like predecessors. The community took notice: unlike the blind yield-chasing of last cycle, people were questioning Ethena’s design and asking how it could offer the 20%+ yield. This healthy scrutiny ironically built trust, as Ethena addressed concerns transparently (e.g. publishing risk disclosures and real-time metrics).

2. Evolution – Multi-Chain Expansion, New Collateral & Products

Ethena’s whirlwind first year saw USDe evolve from a single-chain experiment into a multi-chain, multi-asset protocol while introducing new products.

Adding BTC Collateral (April 2024): By late March 2024, USDe supply grew past the $2B–$3B mark. The team quickly realised that limiting USDe to only ETH perps would bottleneck growth, both in risk and capacity. If Ethena’s hedge positions became too large a fraction of the ETH perp market, funding rates could be pushed down (reducing yield), and liquidity risk would rise (harder to adjust huge positions without moving the market). To avoid this, Ethena moved to support BTC as a collateral asset. This opened up the deep BTC perpetual markets for hedging, greatly expanding USDe’s scalability. It also diversified risk: a shock specific to ETH (e.g. a staking bug) would not completely throw off USDe’s peg.

Ethena enforces a self-imposed cap on its perpetual-swap hedges so that at no point will its short positions in ETH or BTC exceed 10% of that asset’s total open interest. In practical terms, if the ETH perp market has $20B in OI, Ethena will never short more than $2B notional, and the same rule applies on BTC markets. This guardrail ensures that Ethena never overwhelms the market depth, protecting both the funding-rate economics that power sUSDe yields and limiting adverse slippage or funding-rate dilution. The Risk Committee monitors real-time OI metrics via on-chain dashboards, and if trends approach the 10% threshold, Ethena automatically reins in new USDe minting or shifts more collateral into stablecoin buffers until headroom is restored.

Inclusion of Stablecoins in Collateral (mid-2024): Another evolution was Ethena’s approach to “liquid stables” – i.e. holding a portion of reserves in actual fiat stablecoins (USDC, USDT) as a liquidity buffer. Initially, Ethena aimed to be 100% crypto-backed, but the real-world behaviour of users shaped policy. As USDe gained adoption, minters showed a preference to mint and redeem in stable assets (USDC/USDT) rather than volatile ETH/BTC. This makes sense: a market maker swapping USDC for USDe incurs less market risk than using ETH. Thus, Ethena began maintaining ~5% of USDe’s supply as stablecoin reserves. This liquid buffer, though small, proved invaluable during redemption surges. By holding some USDT/USDC, Ethena could meet redemptions without immediately unwinding large hedge positions, thus protecting the peg and revenue. By late 2024, Ethena embraced a dynamic allocation between crypto collaterals (ETH, stETH, WBTC) and stables (USDC, USDT), managed by its Risk Committee. The policy was to “prioritise liquidity and stability” of backing assets, adjusting the mix as market conditions evolved.

For example, after stETH yield declined and a few minor stETH-ETH depeg events in 2023, Ethena scaled back stETH share in favour of plain ETH and stablecoins. By July 2025, the collateral composition behind USDe was a diversified basket: roughly 50–60% crypto (ETH, WBTC, stETH) and ~40–50% stablecoins & cash equivalents, including tokenised money market funds (more on that shortly).

Native Governance Token (ENA) and Incentives: On April 2, 2024, Ethena launched its governance and value-accrual token ENA via a massive retroactive airdrop. $450M worth of ENA was airdropped (one of the largest in DeFi history) to early USDe users, LPs, and campaign participants. The ENA token’s role is twofold: governance (voting on risk parameters, new collaterals, etc.) and fee accrual. Ethena directs 20% of all protocol revenue to buy-and-burn ENA on the open market. Additionally, ENA can be staked (sENA) and, in the upcoming Converge chain (more on it below), will secure the network. The ENA airdrop not only rewarded pioneers but also kickstarted secondary liquidity – ENA quickly reached a multi-billion market cap, giving Ethena a strong treasury for partnerships and security.

Multi-Chain Rollout via LayerZero (H2 2024): Recognising that stablecoin adoption thrives on accessibility, Ethena aggressively expanded USDe beyond Ethereum. In mid-2024, Ethena integrated with LayerZero’s omnichain protocol, turning USDe, sUSDe, and ENA into OFTs (Omnichain Fungible Tokens) that seamlessly bridge across networks. This effectively made USDe chain-agnostic: users on Avalanche, Arbitrum, Polygon, Base, BNB Chain, Gnosis, Optimism and others could mint or swap USDe natively via LayerZero endpoints. Ethena marketed this as “the fastest growing stablecoin ever goes omnichain”, enabling USDe liquidity on every major L1/L2. By late 2024, USDe pools popped up on Arbitrum (Camelot exchange), Avalanche (Platypus, etc.), Polygon, Base and more. This multi-chain push was strategic: it tapped into diverse DeFi user bases and use-cases.

By making USDe ubiquitous, Ethena aimed to position it as a viable alternative to USDC/USDT across ecosystems. Each chain added also brought liquidity impacts: Ethena often bootstrapped initial liquidity pools (sometimes via its reserve fund or incentives). For example, a USDe-USDC Curve pool was seeded, and similar pools on other chains ensured tight peg arbitrage. This omnichain presence enhanced USDe’s peg stability, as arbitrageurs can move USDe across chains to wherever price deviates and profit by rebalancing – a built-in stabiliser. Ethena even implemented a Peg Arb mechanism in its design to arbitrage any sizable peg discrepancies, further reinforcing stability.

Integrations & Use-Cases: Parallel to chain expansion, Ethena forged numerous protocol integrations:

Curve & Balancer (Stablecoin Pools): As early as Q1 2024, USDe was listed in Curve’s stable swap pools, often paired with USDC/USDT for deep liquidity. This gave traders confidence in 1:1 convertibility. Ethena’s reserve provided liquidity and even incentives for a period, quickly driving Curve pool volume into the tens of millions of dollars. By mid-2024, USDe was frequently among the top 5 stablecoins by Curve liquidity on the Ethereum network. Balancer’s stable pools similarly integrated USDe for swaps and boosted yields (via Aura).

Pendle (Yield Trading): Ethena’s yield-bearing sUSDe became an asset on Pendle Finance – users could trade and lock in future yield by splitting sUSDe into principal and yield tokens. Pendle integration (mid-2024) was significant as it validated sUSDe’s yield as composable. It allowed sophisticated users to go long or short Ethena’s future APY, reflecting market expectations of funding rates. This drove more arbitrage and balanced demand: if sUSDe yield was expected to drop, one could sell yield tokens, etc.

Centralised Exchanges & CeFi: By late 2024, several CEXs listed USDe or sUSDe. Bybit was notable – it not only helped hedge Ethena’s positions, but Bybit also offered USDe on its platform for traders (likely seeing volumes from those longing crypto with USDe collateral). Anchorage, a major institutional custodian, onboarded support for USDe by early 2025, a critical step for enterprise adoption.

Lending Markets: Recognising the synergy of a yield-bearing stablecoin as collateral, Ethena pursued lending integration. sUSDe was added as collateral on Aave and many other similar protocols. Risk assessors noted sUSDe’s stable value plus native yield could be attractive for borrow usage (though complexities around its evolving exchange rate were considered).

Payment Rails (TON integration): Perhaps Ethena’s most high-profile integration has been with TON (The Open Network), the blockchain associated with Telegram’s 1+ billion users. In April 2025, Ethena and TON Foundation announced a partnership to bring USDe/sUSDe to Telegram’s native wallet. By mid-2025, Ethena’s sUSDe was deployed on TON as “tsUSDe” (TON Staked USDe). This was deeply integrated: Telegram’s built-in custodial wallet and the non-custodial TON Space wallet both supported tsUSDe for send, receive, and earn. Major TON ecosystem wallets (Tonkeeper, Tonhub, etc.) also integrated USDe. The goal: let everyday Telegram users globally “send, save and pay with a dollar” in-app. To spur adoption, TON Foundation provided a 10% APY boost paid in TON for tsUSDe holders. This incentive, on top of Ethena’s yield, meant Telegram users could earn ~15%–18% on dollar balances, a neobank-like offering that few fintechs can rival. This integration underscores Ethena’s ambition to straddle DeFi and consumer finance: using DeFi yields to power Web2-like experiences (payments, savings) for potentially hundreds of millions of retail users.

3. How USDe opens infinite possibilities

On Pendle, sUSDe is treated as a yield-bearing “underlying asset” that can be tokenised into two tradable parts: Principal Tokens (OT) and Yield Tokens (YT). A user deposits sUSDe into Pendle’s sUSDe market and receives an equal amount of PT and YT. The PT represents your principal claim on sUSDe at maturity, while the YT entitles you to all of the funding-and-staking yield that accrues until that date. From there, you have two main strategies:

Yield monetisation: Sell your YT immediately to lock in today’s implied yield rate as a lump-sum payment, freeing up capital to redeploy elsewhere, while another buyer takes the long-tail yield.

Yield farming: Hold or buy YT if you believe sUSDe’s future APY will rise, then redeem at maturity for a payout greater than what you paid, effectively speculating on yield curves. Meanwhile, you can stake your PT in Pendle’s farm to earn additional protocol incentives or hold it to reclaim your original sUSDe principal plus any leftover yield.

By splitting principal and yield, Pendle lets sUSDe users hedge, speculate, and optimise their positions—turning a once-static staking token into a fully-composable building block in DeFi’s yield markets.

4. Timeline of Key Milestones and Inflection Points:

November 2023: USDe Launch. Concern over high yield sparks industry discussion. Ethena responds with transparency on risks.

March 2024: Peak APY ~67% as funding spiked. Ethena became the highest-earning dApp. USDe market cap crosses $1B.

April 2024: USDe market cap crosses $2B. Total users ~100k+. ENA token Airdrop ($450M distributed). ENA begins trading. BTC collateral added.

June 2024: USDe live on Arbitrum and Polygon via LayerZero. Curve pools see USDe volume surge. USDe passes $3B supply (fastest ever).

Late 2024: Market shifts – crypto rally leads to lower perp funding (some weeks slightly negative). Ethena’s APY compresses (sUSDe exchange rate growth slows). Ethena adjusts strategy. Starts pursuing RWA yields (leading to creation of USDtb) and engaging regulators. USDtb stablecoin quietly launched as Ethena partners with Securitize/BlackRock for a Treasury-backed dollar.

January 2025: sUSDe price peaks ~$1.29.

April 2025: Ethena & Securitize unveil Converge Chain plan. Also, the iUSDe concept was introduced (an institutional-grade sUSDe variant).

April 2025: TON integration announced. USDe = $5B cap; USDtb = $1.4B cap. Reserve Fund >$60M.

June 2025: Ethena engages the SEC for regulatory clarity.

July 2025: Revenue $422M reached. USDe supply ~5.3B and USDtb supply ~1.4B. sUSDe APY rebounding as the market turns. Ethena’s global headcount (still just ~30) and community continue to grow, cementing it as one of 2024/25’s breakout DeFi projects.

5. Risks & Regulatory Headwinds

No project review, especially in finance, is complete without discussing risks. Ethena, for all its innovation, carries a web of risks that must be managed:

Funding Rate Risk: USDe’s engine lives or dies on the basis premium, the funding payments Ethena earns for being short perpetual futures while holding the underlying spot collateral. When the market is bullish and perp prices sit above spot, funding turns positive, so longs pay shorts each interval; Ethena, being short, collects that income, and sUSDe’s APY rises. The real danger lies at the opposite extreme: in a deep or protracted bear market (or during sudden flight-to-cash events), perps can flip below spot, funding goes negative, and Ethena must pay to maintain its hedges. If negative funding persists or spikes hard, the protocol’s net yield can drop toward—or below—zero, eroding the reserve fund and, in a worst-case stretch, shaving a few basis points off the sUSDe exchange rate until conditions normalise. Ethena mitigates this by (1) building a 1%-of-TVL reserve fund from the yield generated and (2) holding collateral that earns independent yield (e.g., stETH rewards, USDtb coupons) to cushion mild inversions.

Liquidation/Custodial Risk: Spot collateral sits with qualified custodians (Copper, Coinbase Custody, etc.) while the corresponding shorts live on CEXs such as Deribit, Binance or Bybit through off-exchange settlement rails. A sudden exchange bankruptcy, custody freeze, or extreme wick that liquidates hedge positions faster than bots can rebalance could punch a hole in backing. The team spreads inventory across venues, maintains excess margin, and keeps “shadow hedges” on secondary venues to re-establish deltas quickly, but the tail risk of an FTX-style failure or coordinated regulatory seizure remains. Ethena’s on-chain reserve covers small impairments; anything larger would trigger a vote on recapitalisation or partial haircut.

Smart-Contract Risk: USDe, sUSDe and soon Converge are governed by Solidity and Nitro contracts—code that, if flawed, can be exploited in minutes. While Ethena has undergone multiple audits (Trail of Bits, Spearbit) and runs continuous bug-bounty programs, no audit can prove the absence of risk; new integrations (LayerZero bridges, reward gauges, validator staking, etc.) constantly widen the attack surface. A critical bug could let an attacker mint unbacked USDe, drain treasury assets or brick redemption functions—jeopardising the peg. Time-locked upgrades, multisig guardians, circuit-breaker pausable modules, etc, reduce, but do not eliminate, that risk.

Regulatory Risk: USDe is neither a classic e-money token (fully cash-backed) nor a pure commodity token; it blends derivatives and staking yields that regulators may classify as securities, collective-investment schemes, or even swaps. A formal SEC ruling that sUSDe is an investment contract could see exchanges delist it and liquidity drain overnight. Likewise, MiCA’s forthcoming “significant EMT” rules might force Ethena to hold 100% in bank deposits, killing the model. The team’s strategy is to (i) open dialogue early (SEC meeting, June 2025), (ii) push regulated variants (iUSDe, USDtb), and (iii) domicile Converge in a jurisdiction with tailored digital-asset statutes (e.g., Abu Dhabi, Bermuda). Yet, policy remains the biggest binary risk on the board.

Competition and Market Perception: Yield-bearing dollars are the new gold rush: Maker’s “NewStable”, Angle’s sEUR+, Levana’s L-Dollar, etc, all compete for the same perpetual-funding and RWA spread. Should a rival deliver similar APY with better UX, higher transparency, or a U.S. licence, USDe could plateau or even lose supply, shrinking fee income and reserve coverage. Conversely, a single publicised peg wobble (even if recovered) can trigger a social-media-fuelled bank-run spiral, as UST holders learned. Ethena therefore invests heavily in real-time dashboards, third-party attestations, and proactive comms—yet reputation is a fragile moat.

Tech & Execution Risks: Launching Converge turns Ethena from a protocol into a full-stack L2 operator. It must ship performant sequencers, cross-domain bridges, MEV defence, validator incentives and on-chain governance—all while running a multi-billion-dollar balance sheet. Feature creep (iUSDe, RWA marketplaces, permissioned sub-nets) and talent bottlenecks raise the odds of missed deadlines or security lapses. Execution missteps (e.g., a buggy bridge or sequencer outage) could erode trust faster than any market event. Keeping the core simple, open-sourcing code, and tapping seasoned infra partners (Arbitrum, Celestia, Chainlink) is vital, but operational complexity will only grow.

These are some other risks that also need to be considered beyond the headline items of funding, custody, contracts, regulation, competition and execution. Oracle and price-feed risk lurk whenever external price data misreports ETH or BTC, allowing the vault to under-hedge or over-redeem. Ethena hardens its oracles with dual Chainlink–Pyth feeds and on-chain sanity checks, yet a feed outage at a critical moment could still distort the peg. Bridge and omni-chain risk arises because USDe, sUSDe and ENA move through LayerZero endpoints; a messaging exploit or replay attack could mint unbacked tokens or strand collateral on a target chain. The team audits each endpoint and imposes mint caps, but the attack surface grows with every new network.

A subtler danger is reserve-fund adequacy: the 1% buffer was modelled on historical drawdowns; a 2008-style shock or exchange insolvency might demand more capital than the buffer and fee-skimming can replenish. Each of these factors, though less dramatic than an outright peg break, can steadily erode confidence if not actively monitored and mitigated.

6. Vision 2028: Ethena’s Place in the Stablecoin Landscape

Projecting out three years, one can envision a few scenarios for Ethena:

Base Case: Ethena successfully launches Converge mainnet by 2026, attracting moderate institutional usage. USDe stabilises around $10–15B supply, USDtb around $20B as more corporate cash comes on-chain. sUSDe yields average ~5% as the market matures and more arb drives funding towards parity with TradFi rates. Ethena becomes a known player, maybe partnering with a big bank or fintech. Regulators permit its operation under oversight; maybe Ethena gets a license in a friendly jurisdiction and is deemed a compliant “crypto money market fund.” It sits alongside USDC, USDT and others as part of a diversified stablecoin ecosystem.

Bull Case: Ethena’s model becomes the dominant form of stablecoin. Crypto markets in 2026–27 are volatile (driving healthy yields), while trust in fiat stablecoins wanes (perhaps due to more bank scares or government restrictions). USDe shoots to $100B+ supply as users globally flock to a self-sovereign dollar that generates an 8%-12% yield. Ethena’s Converge chain hosts a thriving RWA market, effectively a parallel mini Wall Street, with tens of billions in tokenised securities settled in USDe. USDe, perhaps even breaks into the top 5 cryptos by market cap. In this scenario, Ethena may have navigated regulation by working with regulators, maybe the SEC gives tacit approval, or a new law creates a stablecoin charter under which Ethena is grandfathered. The convergence of interest rates happens: by 2028, holding USDe yields may be 6% while U.S. Treasuries yield 5%, meaning capital flows freely through Converge between TradFi and DeFi opportunities (exactly Ethena’s goal).

Bear Case: Ethena faces a major setback – possibly a regulatory ban in the U.S. (e.g., SEC sues calling USDe an unregistered security), causing exchanges to delist USDe and many users to exit. Or a black swan like a CEX default that takes a bite out of reserves, causing a panic redemption and USDe briefly losing peg (say it drops to $0.95 in markets). Confidence could be shaken, and Ethena might scale down temporarily. In such a case, supply could shrink considerably (like UST did, though USDe is redeemable, so it’d unwind more gracefully). However, even in extreme bear cases, Ethena will likely survive in some form – because unlike algorithmic stables, Ethena’s assets don’t evaporate as long as they’re well-managed.

On balance, Ethena’s future will depend on trust. Trust from users that it’s safe and profitable, and trust from regulators that it’s not a systemic risk or scam. So far, Ethena has been transparent about risks: their documentation enumerates funding risk, liquidation risk, custodial risk, exchange failure risk, backing asset risk, stablecoin-specific risks (like peg runs), and margin collateral risks. They’ve implemented mitigations for each (e.g., diversified perps to reduce funding swings, conservative collateral ratios to avoid liquidations, using insured custodians to lower exchange risk, maintaining a reserve fund as insurance, etc.). This proactive risk management is a positive sign.

In conclusion, Ethena’s story is one of innovation meeting execution. It took an idea from a blog and turned it into a multi-billion-dollar reality in under two years. By launching USDe on Ethereum with a carefully chosen collateral mix (ETH and a dash of stETH), Ethena set the stage for a new class of stablecoin – one that is neither fully fiat-backed nor wild algorithmic, but a hybrid drawing strength from crypto markets themselves. It then evolved rapidly: adding BTC collateral to sustain growth, integrating with DeFi and CeFi alike, and proving its resilience under stress. It delivered staggering yields to its users – a clear answer to the global hunger for yield on cash, all while avoiding blow-ups that plagued others. Now, by pushing into its own chain and regulated assets, Ethena is attempting to rewrite the architecture of stable-value finance.

Three years from now, we may very well see Ethena’s USDe and USDtb as fundamental building blocks of the crypto economy, perhaps even bleeding into traditional finance. Imagine governments or central banks taking note that an autonomous protocol is effectively offering an alternative dollar system at scale. It’s not far-fetched; already, USDe is forcing conversations in policy circles. Ethena stands at the vanguard of stablecoin 2.0 – yield-bearing, multi-chain, and bridging worlds. If it navigates the narrow path of innovation and compliance, Ethena could become to global liquidity what Eurodollars were in the 20th century: a massive, parallel monetary system operated outside traditional banking, yet integral to it. In that sense, Ethena’s story is more than just DeFi – it’s potentially a chapter in the evolution of money itself, one where internet-native dollars compete and converge with nation-state dollars. The coming years will tell whether that promise is fulfilled, but today, Ethena has undeniably moved the needle toward that future.