The Hyperliquid Phenomenon: How 11 People Beat NASDAQ

The origin story, tech, philosophy, and tokenomics flywheel powering DeFi’s fastest and largest exchange

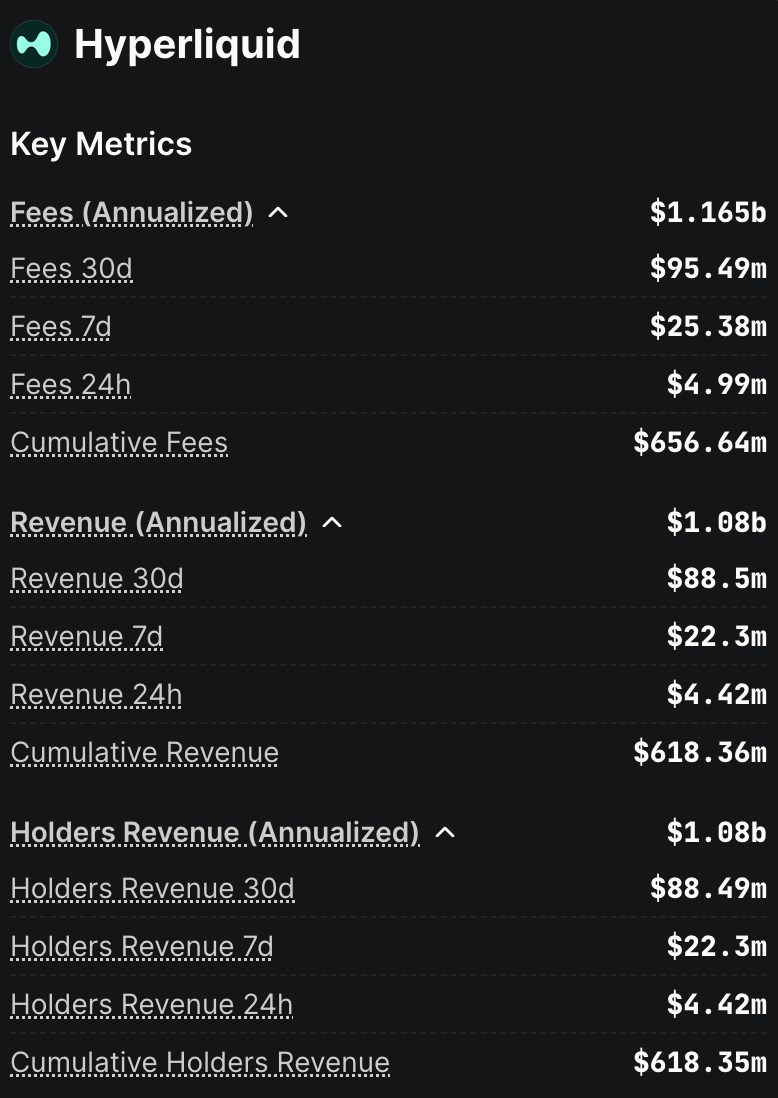

Over the last 30 days or so, Hyperliquid generated approximately $88.5m of revenue (≈US$1.08bn annualised), putting it broadly in line with Nasdaq’s Market Services net revenue of about $102m per month in Q2-2025. But Hyperliquid achieved it with just ~11 core contributors, which equates to roughly $100M of revenue per employee, the highest for any company. Hyperliquid delivers on-chain trading speeds once thought impossible, while handling tens of billions in daily volume—all while remaining non-custodial and community-owned.

This report provides a comprehensive deep dive into Hyperliquid’s journey: its origin story and team ethos, the technical breakthroughs underpinning its performance, the HYPE tokenomics (including one of DeFi’s largest airdrops), governance evolution, competitive landscape, and what the future holds. By the end, it will be clear why Hyperliquid has captured everyone’s imagination.

Origins: A Small Team with a Big Vision

Hyperliquid’s story begins with its quietly brilliant founder, Jeff Yan. A Palo Alto-born physics prodigy and Harvard graduate, Yan cut his teeth building ultra-low-latency trading systems at Hudson River Trading, a top high-frequency trading firm. There, he learned how to execute thousands of trades per second and develop rigorous market-making strategies. By 2018, he was dabbling in crypto, even attempting a prediction market startup that ultimately failed amid regulatory hurdles. But it was the November 2022 collapse of FTX that galvanised Yan to pursue a new vision. Seeing billions of user funds evaporate on a centralised platform convinced him that the future belonged to on-chain exchanges that users could trust.

“We saw the problems with FTX firsthand... People realized that crypto was supposed to be a fun game, but it wasn’t until something bad happened that it stopped being a fun game,” Yan recalled. Determined to build a safer alternative, he made a bold decision: create a custom blockchain purpose-built for trading, one that could match the speed and experience of a CEX without compromising self-custody.

Yan leveraged his own funds (from operating a successful crypto market-making firm, Chameleon Trading) to bootstrap development, rather than seeking venture capital. This self-funded approach was deliberate—Yan believes large VC stakes in networks become “a scar on the network” that can harm long-term alignment. By 2023, he had assembled a tiny, tight-knit team (fewer than a dozen people) and begun coding what would become Hyperliquid’s Layer-1 blockchain.

The team operated in stealth and launched Hyperliquid’s exchange in late 2023 with little fanfare—no big fundraising announcements, no influencer campaign. An “Alpha” version went live around December 2023, offering perpetual futures trading with USDC as margin. Early adopters trickled in, finding a platform that “just worked”: sub-second trade execution, an intuitive interface, and none of the usual friction of on-chain trading. Within six months, Hyperliquid’s volumes exploded, and it became a top-20 blockchain by TVL. By mid-2024, daily trading volumes had reached the billions, and Hyperliquid quietly became the largest decentralised derivatives exchange.

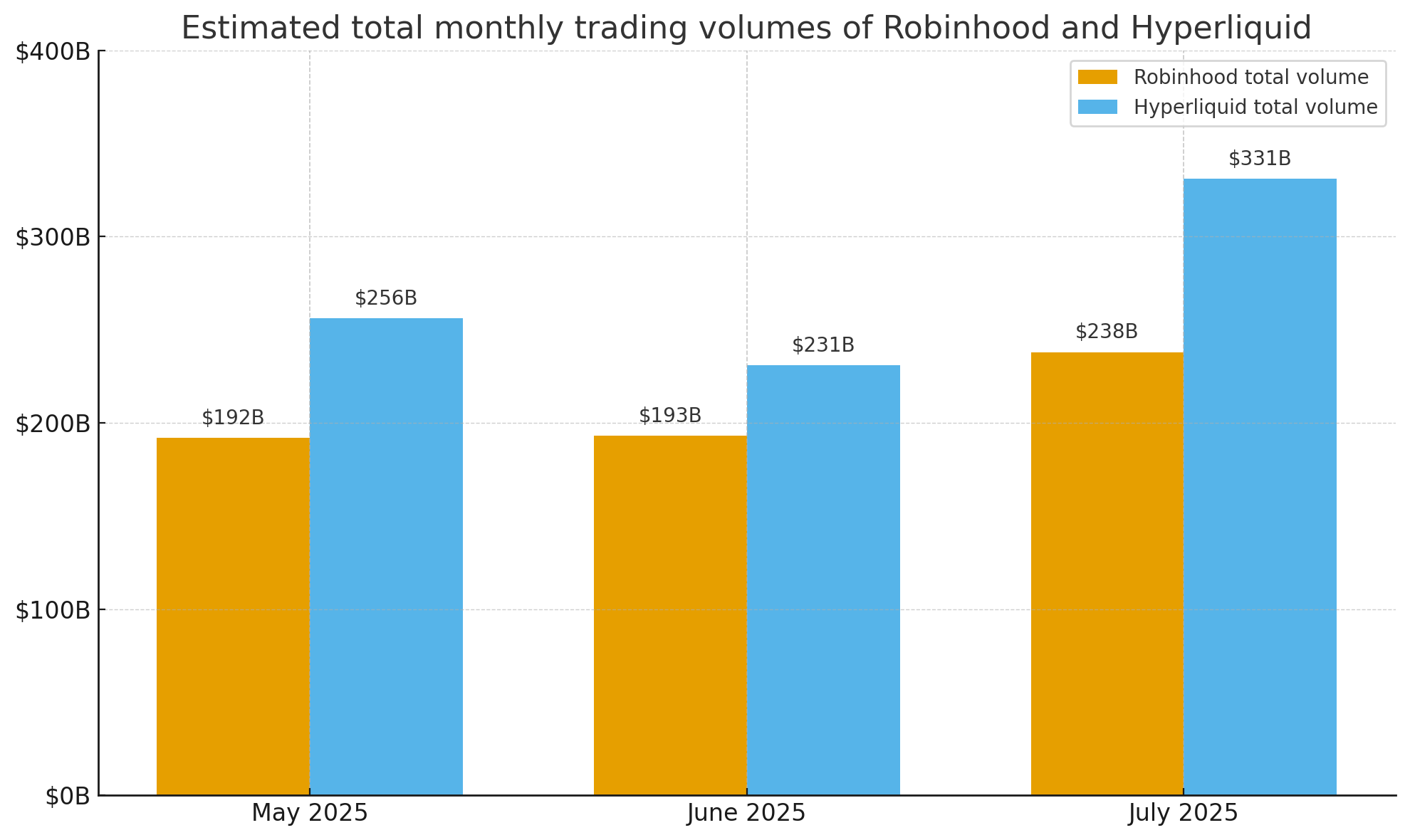

Those early metrics were staggering for such a small operation. Over the 12 months through late 2025, Hyperliquid facilitated about $1.8 trillion in trading volume—over 10% of global crypto perpetual futures activity—with more than 200,000 active users trading each day. Revenue climbed into the hundreds of millions (more on that later). Perhaps most impressively, by July 2025, Hyperliquid’s monthly trading volume (~$330 billion) surpassed Robinhood’s, a traditional retail brokerage, for the third month in a row. It’s a feat that has redefined what a lean startup can do in crypto—Hyperliquid proved that a small, highly focused team can out-build and out-innovate far larger organisations.

A Philosophy of Focus and User-Centricity

Part of Hyperliquid’s magic lies in the philosophy instilled by Yan and his co-founders. Jeff Yan is known for being soft-spoken and avoiding the spotlight, but his principles speak loudly. “If something can be built by someone else, it should be built by someone else,” he often says. This captures Hyperliquid’s ethos: focus on what you’re uniquely good at (in their case, the core trading engine and blockchain), and empower the community or other builders to do the rest. Indeed, Yan intentionally kept the team small and hiring bar high—“Hiring the wrong person is worse than not hiring at all,” he noted, emphasising cultural cohesion over rapid expansion.

Rejecting venture capital was another intentional choice. Hyperliquid has zero VC investors; ownership was aligned with users from day one. Yan distributed protocol revenue back to the community (over $25 million early on) instead of allocating fees to the team. The project didn’t even pursue major centralised exchange listings for its token at launch, as Yan preferred to focus on product and organic community growth over hype. This independence gave Hyperliquid the freedom to prioritise users’ interests without investor pressure for short-term returns.

Crucially, Hyperliquid’s team also fostered a “ship, fix, own it” culture. A notable example came on July 29, 2025, when an API outage disrupted order execution for 37 minutes. The very next day, the team reimbursed affected traders ~$1.99 million from its own funds. In DeFi, such prompt and voluntary compensation is almost unheard of. It demonstrated Hyperliquid’s commitment to users and willingness to take responsibility—further building trust in the platform.

All these elements—technical excellence, humble yet bold leadership, user-first economics, and responsive operations—created a narrative that captured the crypto community’s imagination. Hyperliquid wasn’t just another exchange; it felt like a movement to build a fairer, faster financial system from the ground up. Next, we will dive into the technical innovations that make that system possible, and how a DEX can indeed rival the speed of Wall Street.

Technical Innovations: Building a Nasdaq on-Chain

Hyperliquid’s ability to offer a CEX-like experience in a decentralised setting comes down to its groundbreaking technical architecture. At its core, Hyperliquid is an app-specific Layer-1 blockchain engineered for performance. Let’s break down the key innovations:

Custom Chain with Dual Engines: Hyperliquid runs on its own Layer-1 network, split into two tightly integrated components: HyperCore and HyperEVM. HyperCore is the trading engine—it manages the central limit order books, trade matching, margin accounting, and liquidations fully on-chain. HyperEVM is an EVM-compatible smart contract layer that operates in parallel, sharing the same blockchain and consensus. This dual architecture means Hyperliquid can process trades at incredible speed in HyperCore, while still allowing general-purpose smart contracts and DeFi applications on HyperEVM that can interact natively with the exchange state. Both layers share one source of truth and finality.

HyperBFT Consensus (Speed and Finality): Under the hood, Hyperliquid uses a proprietary consensus protocol called HyperBFT, inspired by the HotStuff Byzantine fault tolerance model. This consensus achieves sub-second finality (~0.2 seconds) and can handle up to 200,000 transactions per second, according to the team’s benchmarks. In practice, median trade latency on Hyperliquid is about 0.2s (with 99th percentile under 0.9s)—effectively on par with top CEXs. Achieving this required deep optimisation of the consensus and networking layer. Initially, Hyperliquid even built on Tendermint for its speed, before developing HyperBFT in Rust to push performance further. The result is a chain that finalises trades near-instantly, eliminating the clunky pending/confirmation delays users often associate with blockchains.

On-Chain Orderbook with No Off-Chain Tricks: Unlike many DEXs that rely on automated market makers (AMMs) or hybrid designs (off-chain matching with on-chain settlement), Hyperliquid keeps everything on-chain in real-time. Every order resides on the blockchain (within HyperCore’s state), and the matching engine itself runs as part of the chain’s execution. Price-time priority is enforced deterministically by the blockchain, not by any off-chain matching service. This pure on-chain approach is a massive technical challenge—one reason earlier projects shied away from it—but it yields huge benefits in transparency and composability. Any decentralised app can plug into Hyperliquid’s order books via on-chain calls, and users retain custody at all times. Notably, Hyperliquid proved that an on-chain central limit order book can have tighter spreads and better price discovery than AMMs, thanks to efficient market-making and zero latency arbitration with CEX prices.

User Experience Optimisations: Trading on Hyperliquid feels as smooth as on a CEX. There are no gas fees for trades—users aren’t paying Ethereum-style gas for each order. Instead, the platform charges standard trading fees (which are low and tiered by volume/staking status) while abstracting away transaction costs. This was achieved by the custom chain design; Hyperliquid can subsidise or eliminate gas for certain actions, and it likely batches many operations within blocks. The result is that placing an order on Hyperliquid doesn’t require dealing with wallets or gas every time. Hyperliquid even offers conveniences like email-linked wallets for newcomers, and advanced order types (stop-loss, take-profit, etc.) similar to Binance or Coinbase Pro.

Robust Infrastructure (Bridging and Oracles): To bring assets onto its chain, Hyperliquid integrated secure bridging solutions. It built a Solidity-based Ethereum bridge (audited twice) governed by Hyperliquid’s validators. It also adopted Circle’s Cross-Chain Transfer Protocol (CCTP) to allow native minting/burning of USDC on Hyperliquid without relying on conventional bridges. This significantly reduces bridge risk for the primary stablecoin used on the platform. For price oracles, instead of relying on third-party feeds, Hyperliquid’s model draws from aggregated prices of top CEXs for index calculations—a robust approach to keep perpetual prices in line with global markets. Additionally, features like self-trade prevention and robust price indices are built in to prevent manipulation and ensure fair liquidations.

Hyperliquidity (Automated Liquidity for New Tokens): One innovative component is Hyperliquidity (HIP-2), which is essentially an on-chain market-making algorithm baked into the protocol. Inspired by Uniswap’s automated liquidity pools, Hyperliquidity automatically places a grid of orders on new spot markets (against USDC) to bootstrap liquidity for tokens that are newly listed or have low activity. This is done as part of the blockchain’s block logic (no off-chain operator), ensuring even nascent markets have some depth. In effect, Hyperliquidity acts like a decentralised designated market maker, maintaining a 0.3% spread around a reference price and updating orders every few seconds. It’s currently used for spot assets launched via HIP-1 (Hyperliquid’s token standard for new assets). This clever mechanism means new communities can list tokens without immediately attracting big market makers—the protocol itself helps get things started, and then steps back as organic liquidity providers enter.

Permissionless Market Creation (Builder Codes—HIP-3): Hyperliquid is not trying to list every asset itself; instead, it opened the door for external builders to deploy markets. HIP-3 introduced builder-deployed perpetuals, allowing anyone to create a new perpetual futures market on Hyperliquid’s infrastructure. A developer (or market builder) needs to stake some HYPE and can then launch a perp for, say, a specific token or even a non-crypto asset, with the ability to earn a share of fees from that market through fee sharing, something most L1s or DEXs don’t offer. This is part of Hyperliquid’s ethos of composability—the team built the core platform, but others can permissionlessly extend it. In practice, by 2025, we have seen community-contributed markets and even experimental assets like “Hyperps”, which are perpetuals on unusual indexes, deployed on Hyperliquid.

Open Market Making via HLP Vault: Unlike typical exchanges that rely on a few professional market makers, Hyperliquid crowdsourced liquidity provision through the Hyperliquidity Provider (HLP) vault. The HLP is a vault where anyone can deposit assets (primarily USDC) to be used by the protocol for market making and covering liquidation losses. The vault operates a delta-neutral strategy: it provides quotes and takes the other side of trades, earning trading fees and funding payments over time. Contributors to HLP effectively become passive liquidity providers to all markets and share the profits (and losses) of the vault’s activity. Historically, this has yielded around 6–8% APY to depositors, and at its peak, the HLP had over $500 million, providing deep liquidity across Hyperliquid’s books. By making market-making permissionless and transparent, Hyperliquid reduced dependence on insider deals that are common on exchanges. It’s worth noting that only ~7% of trading fees go to HLP rewards (with the rest used for buybacks, discussed later), but even that has been sufficient to attract substantial capital due to the high volumes.

Collectively, these technical choices and innovations enabled Hyperliquid to achieve something unprecedented: full on-chain trading at scale. Users get the performance of a centralised exchange—fast matching, advanced order types, high leverage (up to 40x), tight spreads—while transacting on a public blockchain where they hold their own keys. Liquidity on Hyperliquid became comparable to major centralised platforms, with order book depth often matching Binance or Coinbase for similar pairs. In fact, by early 2025, liquidity was so deep that institutional traders began noticing that Hyperliquid offered institutional-grade execution without counterparty risk.

It’s important to appreciate how Hyperliquid’s success challenged the status quo. Before, one might have assumed you needed a new monolithic base layer (like Solana) or an Optimistic Rollup to get high-speed trading. Hyperliquid instead built an application-specific chain that outperformed many multi-purpose chains. Its throughput up to 200k TPS and ~0.2s finality means it can, in theory, rival the transaction capacity of Nasdaq or the NYSE. Little wonder that observers started calling Hyperliquid the “Nasdaq of DeFi.” The difference: Nasdaq is run by a large corporation and serves brokers; Hyperliquid is run by a small community-centric team and serves anyone with a crypto wallet.

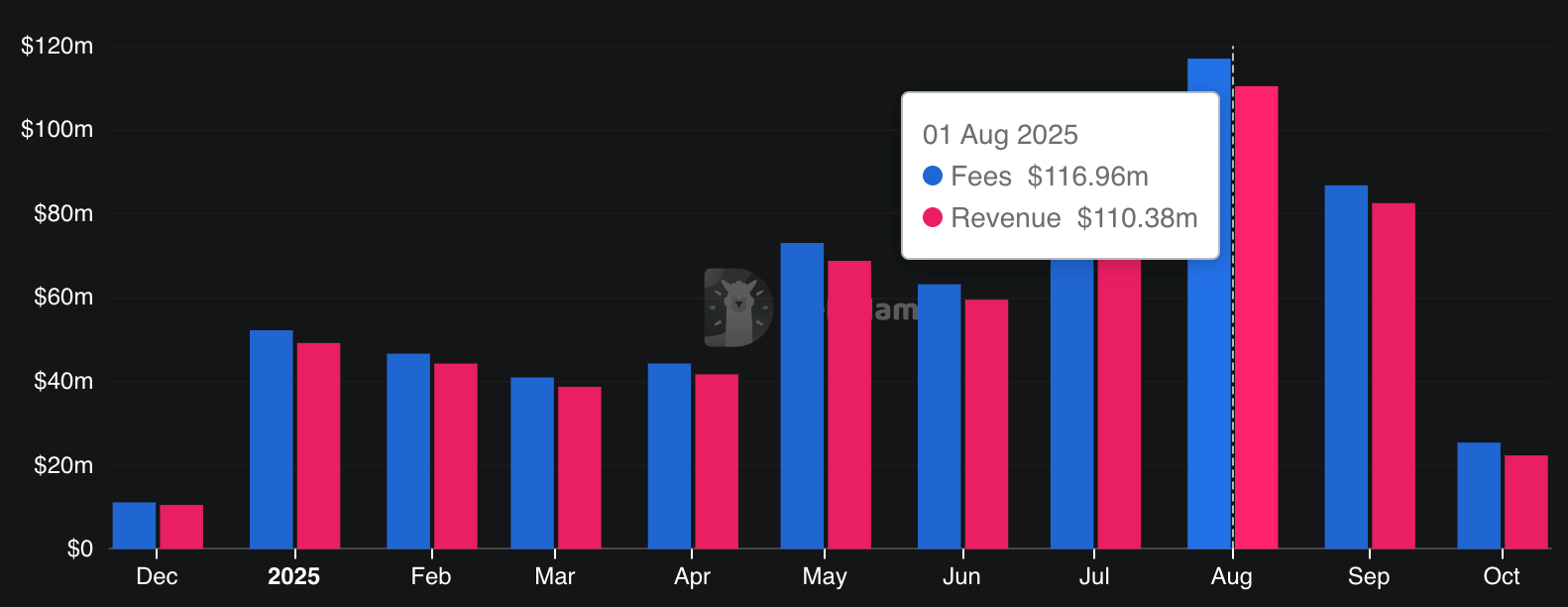

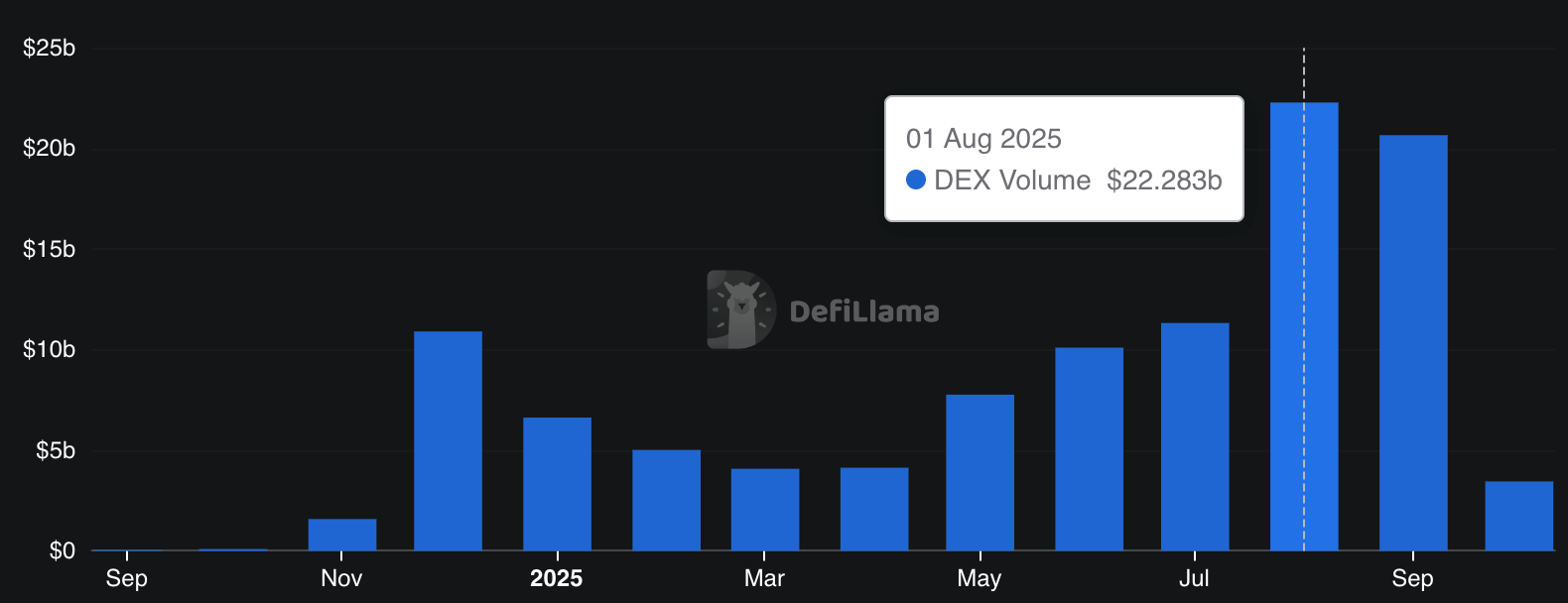

To illustrate Hyperliquid’s growth, consider the images below, which show the platform’s protocol volume and fees over time. It highlights Hyperliquid’s meteoric rise, where monthly volume now consistently surpasses $20B, while generating over $100M in fees—all handled on-chain with sub-second finality.

Tokenomics & Community: The HYPE

Hyperliquid’s technological prowess is only part of the story. Equally important is how it distributed ownership and aligned incentives via its native token HYPE. The launch of HYPE was a watershed moment in DeFi, executed in a way that richly rewarded the community and set Hyperliquid on a path of sustainable, user-driven growth.

A Billion-Dollar Airdrop

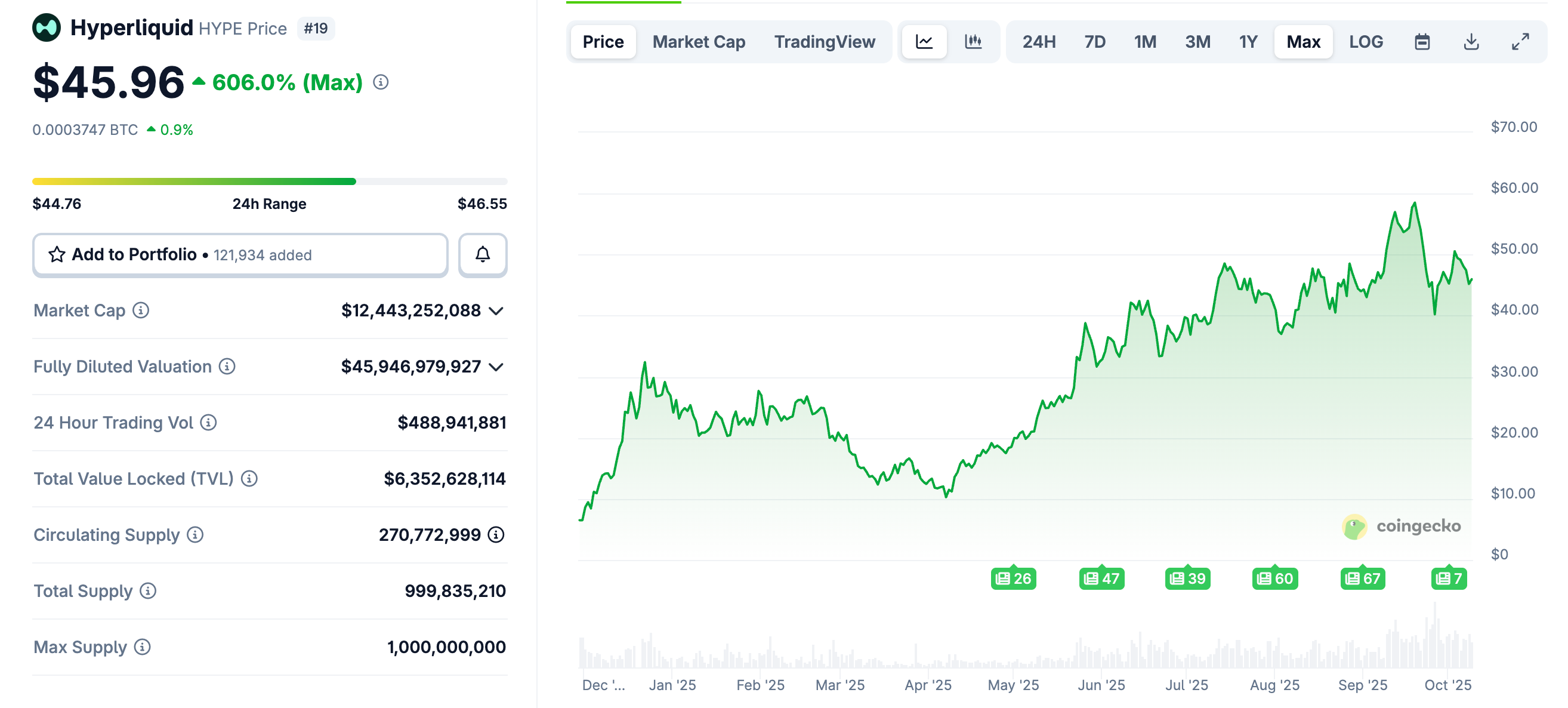

After running successfully without a token for about a year, Hyperliquid introduced the HYPE token via a “genesis airdrop” on November 29, 2024. Rather than a typical token sale or heavy insider allocation, Hyperliquid literally gave away a huge portion of its supply to early users. Specifically, 310 million HYPE (out of a maximum supply of 1 billion) were distributed to eligible community members during this event. At launch, HYPE was priced around $3.90, making the initial distribution worth approximately $1.2 billion. And that was just the beginning—within hours of trading, HYPE’s price surged over 60%, and by a few days later, it hit nearly $10. In fact, at its peak of ~$9.80 shortly after launch, the airdrop’s value reached $2.7 billion, arguably the largest DeFi airdrop ever by total value.

So who got these tokens? Hyperliquid’s ethos of “community first” was evident in the criteria. Only about 94,000 addresses were eligible for the airdrop, which is a relatively small cohort (for comparison, Uniswap’s famous 2020 airdrop went to over 250k addresses, and Arbitrum’s 2023 airdrop to 625k+). This wasn’t a mass giveaway to anyone who clicked a faucet—it was targeted to users who had meaningfully interacted with Hyperliquid during its early phases. The team had run a points program from November 2023 through November 2024, where users earned points each week based on trading volume, liquidity provision, referrals, and other contributions. Those points were used to allocate HYPE in the airdrop. In essence, the more you used and supported Hyperliquid early on, the more HYPE tokens you received.

The distribution stats are striking: the average recipient got ~2,915 HYPE, which at the post-launch peak price was worth about $28,500. (Even at the initial $3.90 price, that was ~$11,000—nothing to sneeze at.) The median user received ~64.5 HYPE, worth around $630 at peak values. This disparity shows that while many users got a few hundred dollars worth, the power-users and top liquidity providers earned life-changing sums. The largest single allocation was a whopping 970,000 HYPE tokens to one address—at one point valued around $9.56 million. Clearly, some heavy traders who likely provided enormous volume/liquidity were handsomely rewarded.

Crucially, there were no tokens allocated to VCs, private investors, or even to market-making firms in this genesis event. Hyperliquid’s token distribution was 100% community and team. To break down the initial token allocation (per the Hyperliquid Foundation’s announcement):

31.0%: Genesis Airdrop to Users: 310,000,000 HYPE for the community at launch (fully unlocked). Any portion not claimed would be rolled into future community rewards (indeed, data suggests about 274M were actually claimed, with the rest unclaimed).

38.888%: Future Emissions & Community Rewards: ~388,880,000 HYPE reserved for ongoing incentives (liquidity mining, trading rewards, etc.) over the coming years. These remained unminted to be emitted gradually.

23.8%: Core Contributors (Team): ~238,000,000 HYPE allocated to founders and core team, but with strict locks—a 1-year cliff after genesis and vesting extending until 2027–2028 or later. The team cannot touch these tokens until at least the end of 2025, and most will vest over 4+ years. Notably, the genesis airdrop explicitly excluded the team accounts (so team members who also used the platform didn’t double-dip).

6.0%: Hyper Foundation Treasury: 60,000,000 HYPE for the foundation’s budget. This is presumably for development, marketing, and ecosystem grants over time.

0.3%: Community Grants: 3,000,000 HYPE earmarked for grants to developers/projects building on Hyperliquid.

0.012%: Hyperliquidity Incentive (HIP-2): 120,000 HYPE set aside to seed the Hyperliquidity program. This tiny allocation was effectively used to bootstrap the on-chain liquidity pool mechanism for new tokens (a technical detail, but included for completeness).

In summary, about 76.2% of HYPE’s supply was designated for the community (either immediately or via future emissions), while 23.8% went to the team (locked). This is arguably one of the most user-centric token distributions in crypto history. It’s only in DeFi that we see billions of dollars handed to a community of users as a reward for their participation—and Hyperliquid’s airdrop ranks at the very top of such events alongside Arbitrum’s 2023 airdrop (which was ~$1B+ value).

The immediate effect was an outpouring of goodwill and buzz. Hyperliquid didn’t just create millionaires; it cultivated a legion of loyal users who now had a stake in the platform’s success. Forums lit up with stories (some users turned a few months of active trading into five or six-figure windfalls), and Hyperliquid’s reputation grew as “the real deal”—a project that truly put its community first, in stark contrast to cynical token launches where insiders reap most of the rewards.

HYPE Utility and Market Performance

HYPE isn’t just an airdrop token; it has integral utility in Hyperliquid’s ecosystem. First, it’s the staking asset for validators in Hyperliquid’s proof-of-stake network. Running a validator node requires staking a significant amount of HYPE (10,000 tokens self-delegated was the original threshold). This secures the HyperBFT consensus and allows HYPE holders to participate in block production (and earn staking rewards). Many community members who received HYPE likely rolled some into staking, further decentralising the network.

Second, HYPE is the gas token for HyperEVM, the smart contract layer. Much like ETH is gas on Ethereum, when deploying or calling contracts on Hyperliquid’s chain, fees are paid in HYPE. Given that HyperEVM launched in February 2025 and has been gaining traction (e.g., Phantom Wallet’s integration, new dApps), this creates organic demand for HYPE as on-chain activity grows.

Third, HYPE represents governance power. Hyperliquid Improvement Proposals (HIPs) and other governance votes are generally influenced by HYPE holdings (details of the governance process are evolving, but HYPE is the de facto governance token). This means holders can help steer protocol parameters, feature upgrades, and treasury usage. For example, decisions like adjusting fee distribution or supporting new incentives would involve the HYPE community voting.

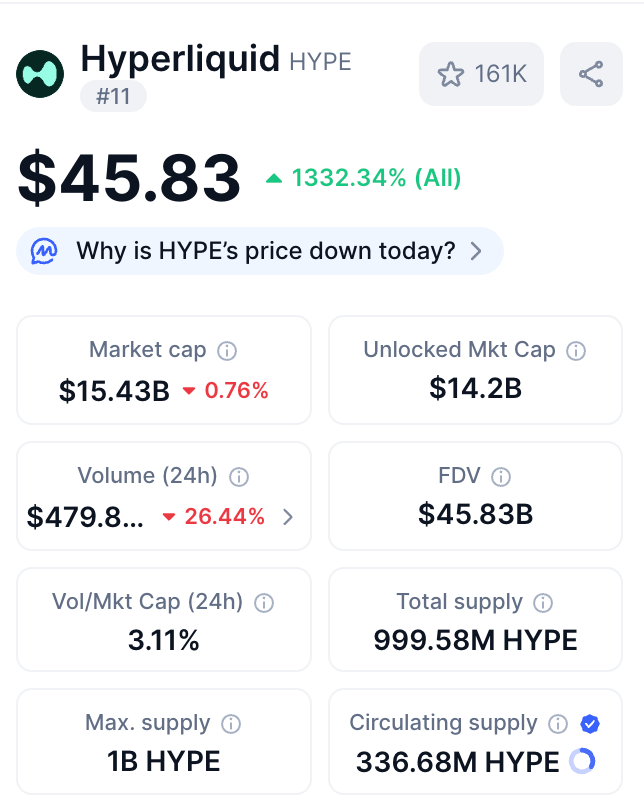

On the market, HYPE’s performance post-launch was impressive. After the initial spike to ~$6 and a quick climb to ~$9, the token settled and then embarked on a steady uptrend in 2025. By August 2025, HYPE hit all-time highs above $50, reflecting hyperbolic growth in platform usage and the impact of its aggressive buyback model (more on that next). That price represented roughly a 15x increase from its late-November debut at around $3. Even as only about one-third of the supply was circulating (the rest being in future emissions or locked), HYPE’s fully diluted valuation reached the $40–50 billion range by late 2025. Analysts at ByteTree noted the strong fundamentals—record fee generation, dominant market share—but also cautioned about the high valuation and upcoming token unlocks for the team (scheduled from November 2025 onward). These are valid concerns: a fully diluted $50B+ is lofty, and the market will be watching how the token supply dynamics play out. We’ll discuss one major proposal to address this (a supply cut) in the governance section.

Before that, however, it’s crucial to understand what might be Hyperliquid’s most unique token feature: its dual deflationary design of continuous buybacks and burns. This mechanism has turned HYPE into a cash flow-driven asset more akin to a stock with buybacks than a typical inflationary reward token.

Buybacks, Burns, and Sustainability

Hyperliquid’s revenue model is remarkably straightforward: it charges trading fees (and small swap/spread fees via HLP) just like any exchange. But what it does with those fees is what sets HYPE tokenomics apart. Instead of funnelling fees to company profit or even directly to stakers (as a dividend), Hyperliquid uses the vast majority of its revenue to buy its own token on the open market and permanently remove it from circulation. This is executed via an on-chain treasury mechanism known as the Assistance Fund.

Assistance Fund: Turning Volume into Buy Pressure

Every time traders pay fees on Hyperliquid, those fees (in USDC or other base assets) are automatically routed to the Assistance Fund. According to on-chain data, a whopping 93% of all protocol fees go into the Assistance Fund, while the remaining ~7% go to reward HLP vault depositors. In fact, Hyperliquid’s fee distribution was recently adjusted to be even more aggressive: in a coming update, 99% of fees will go towards the Assistance Fund’s buybacks, with just 1% to HLP incentives. Essentially, nearly every dollar of fee revenue is used to buy back HYPE from the market.

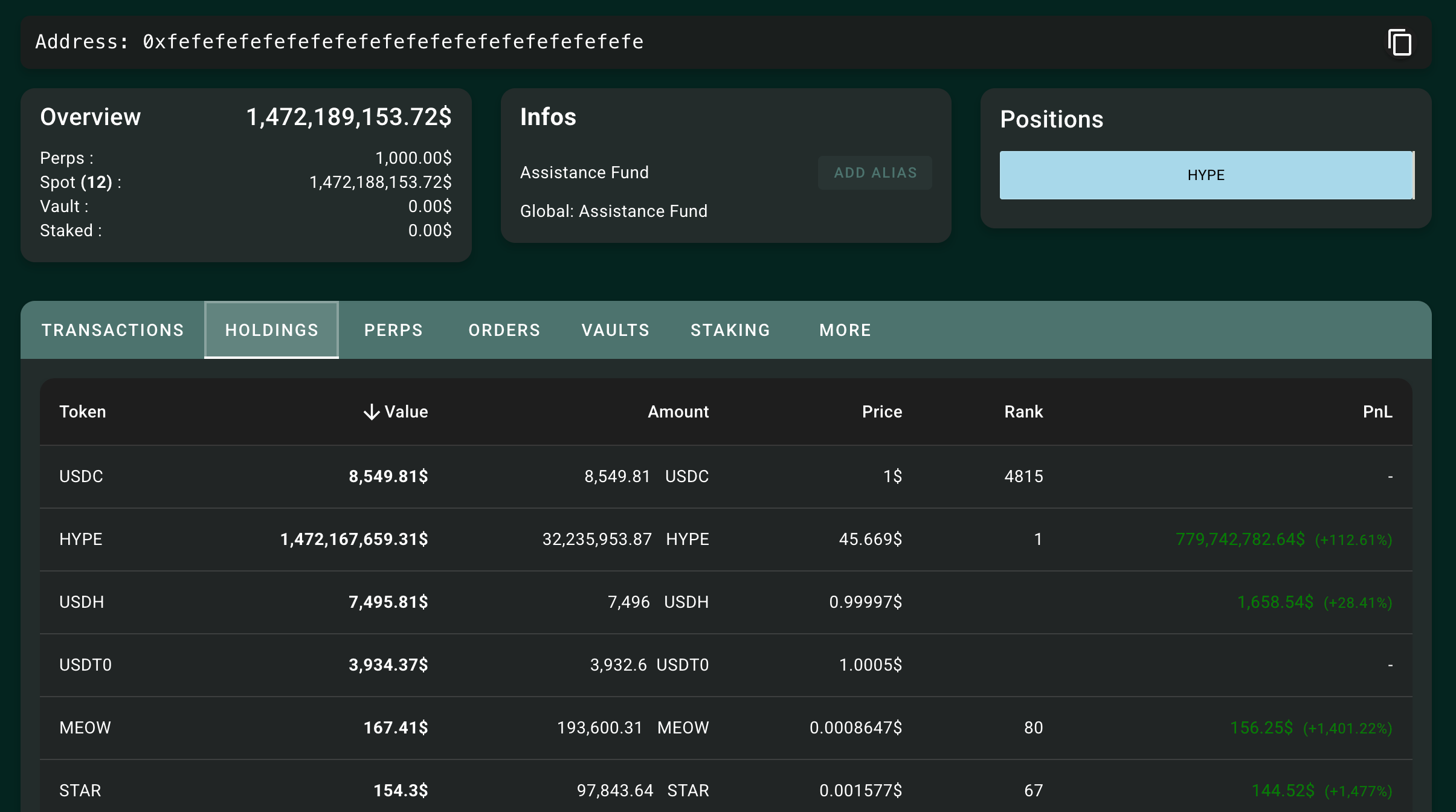

How does it work? The Assistance Fund is implemented as an on-chain entity (a system-owned address 0xfefefefefefefefefefefefefefefefefefefefe on the Hyperliquid chain) that accumulates the fees and regularly executes buy orders for HYPE. These purchases occur on Hyperliquid’s own order book (so the fund is essentially a constant bidder for HYPE using the revenue). The acquired HYPE tokens are then held by the Fund. Importantly, the fund is programmatic and governed by consensus rules—it can’t be arbitrarily moved by a rogue actor; using its funds in any other way (like in emergencies) would require a quorum of validators. In effect, tokens held in the Assistance Fund are out of circulation unless a community/chain decision is made to use them (and currently, the only use case is to burn them or hold them as insurance). This mechanism is often described as buyback-and-burn, since the effect on circulating supply is the same as if they were immediately burned. And indeed, Hyperliquid has signalled that these tokens are earmarked to reduce supply—they have even referred to it as burning in public commentary. Whether held by the fund or sent to a burn address, the key is that those tokens are not hitting the market again under normal conditions.

The scale of these buybacks has grown in tandem with Hyperliquid’s volume. For example, in August 2025, Hyperliquid saw a record $100+ million in fees. “Much of those earnings,” notes a CoinDesk report, “are funnelled directly into purchasing HYPE on the market through Hyperliquid’s Assistance Fund”. And we can see the impact: the fund’s holdings swelled from 3 million HYPE in January 2025 to 32.2 million HYPE by the end of September 2025. At that time, 32.2M HYPE was worth over $1.47 billion (with HYPE around $45). That represents ~10% of the total supply that had been repurchased and effectively burned in about 9 months. In one 30-day window, the fund spent $106M on buybacks at an average price of $42.8 per HYPE. Cumulatively, by late 2025, Hyperliquid had conducted over $1.2 billion in buybacks, with daily buyback volume often around $1M and single-day peaks above $10M.

This dual-deflationary mechanism—organic fee-funded buybacks combined with token burns—has created a powerful flywheel for HYPE’s value. As trading volume increases, more fees flow into buying HYPE, which pushes the price up (all else equal) and reduces circulating supply, making HYPE more scarce. That, in turn, can increase the token’s market cap and community confidence, attracting more users and traders to the platform (since a higher HYPE price often reflects a healthy platform). More traders mean more volume, and the cycle reinforces itself. It’s analogous to a company that uses all profits to buy back stock from the open market: it directly returns value to holders by shrinking the supply. Unlike some exchange tokens that simply give fee discounts or pay out a dividend, Hyperliquid’s approach is to pump value back into the token via continuous market operations. This is reminiscent of what CEXs like Binance (BNB) or Bitfinex (LEO) have done with buy-and-burn programs, but Hyperliquid has taken it to another level by hardwiring it on-chain and dedicating virtually all revenue to it.

All that said, with success came new challenges—for instance, the FDV (fully diluted valuation) of HYPE soared to ~$45B while the circulating market cap was around $14B, creating an “inflationary illusion” gap. This is because ~421M tokens were still unminted (future emissions) and ~32M in the Assistance Fund were not technically removed, which made FDV look much larger than the actually circulating supply.

The Great Supply Cut Debate

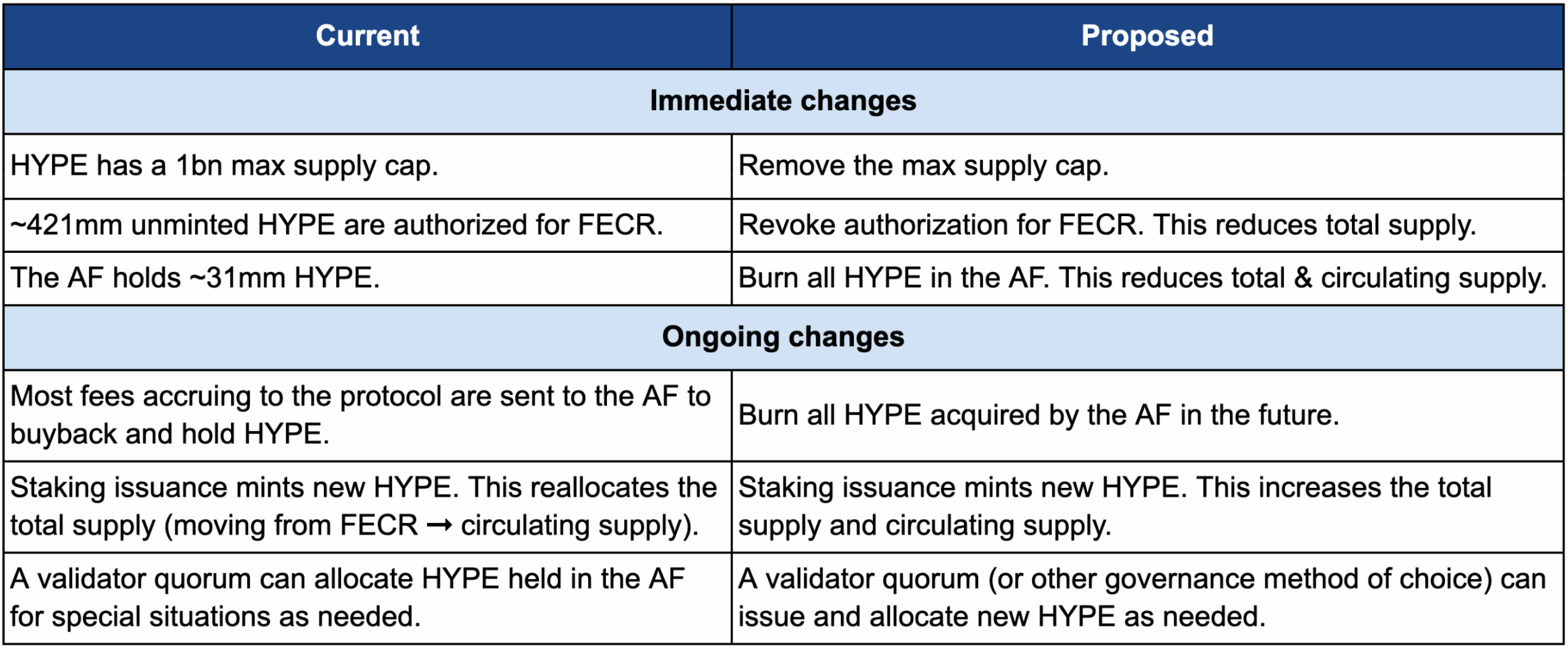

To address this perception (and the impending unlock of team tokens), a dramatic proposal was introduced in September 2025: cut HYPE’s total supply by 45%. Crypto asset manager DBA and researcher Hasu co-authored a plan to burn 452 million HYPE tokens that were not in circulation. Specifically, they suggested permanently revoking the 421M unminted community reward tokens and the 32M tokens held by the Assistance Fund (since those had accumulated as bought-back reserves). This would eliminate those tokens from the supply, thereby aligning the max supply closer to the current circulating amount. It would also remove the notional 1 billion cap, giving flexibility to reintroduce incentives later if needed (via governance) without confusing the accounting.

Supporters argue this would instantly right-size HYPE’s valuation metrics, making it more palatable for institutional investors. It would also cement HYPE’s scarcity, since essentially all “hidden inflation” gets nixed, and future emissions could be governed more transparently. On top of that, the proposal points out that organic burn mechanisms (trading fee buybacks, HyperEVM gas burns, etc.) are already reducing supply gradually. This one-time cut would be like a decisive accounting cleanup, echoing moves like Ethereum’s EIP-1559, which made ETH deflationary.

Of course, there are risks and debates. Opponents worry that burning the Future Emissions reserve might limit Hyperliquid’s ability to incentivise growth down the line (less “ammo” to reward liquidity mining, developers, or other campaigns). Also, burning the Assistance Fund tokens could reduce the safety net for black swan events or major losses (since those tokens could have been used in emergencies). It’s a trade-off between aggressive deflation and retaining flexibility. There’s also the psychological aspect: a 45% supply cut could cause short-term volatility or confusion, especially with a large token unlock for team tokens looming (238M team tokens start vesting after November 2025). The community will have to weigh these factors carefully. As of this writing (October 2025), the proposal was under heated discussion but not yet executed, awaiting a formal governance vote.

No matter how that turns out, the overarching picture is that Hyperliquid’s tokenomics are distinctly sustainability-focused. No yield farming emissions are diluting HYPE’s value (the remaining community rewards are earmarked for strategic purposes, not indiscriminate farming). The team has shown willingness to forgo short-term profit (zero fee cut for themselves) to bolster long-term token value. And the community is now actively steering token policy via governance—a sign of healthy decentralisation.

Speaking of decentralisation, let’s turn to how Hyperliquid is progressively handing over the reins to its community and what governance in the Hyperliquid ecosystem looks like.

Toward Decentralisation: Governance, Ecosystem, and Challenges

From the outset, Hyperliquid aimed to be more decentralised over time despite its high-performance nature. This is a delicate balancing act: the protocol must maintain its technological edge (often easier with a tight-knit team) while distributing control and fostering an open ecosystem. Here’s how Hyperliquid is navigating that journey:

Validators and Security

Hyperliquid’s blockchain is secured by a network of validators (stakers) running HyperBFT consensus. The project launched with permissionless validator participation—anyone could spin up a node and join the active validator set by self-staking the required HYPE (initially 10k) and attracting delegations. This is in contrast to some other app-chains that start centralised. By allowing community members to become validators from day one, Hyperliquid signalled its intent not to control the network ledger single-handedly.

In practice, because Hyperliquid’s throughput is so high, running a validator likely requires strong hardware and technical know-how. The barrier (plus needing $100k+ worth of HYPE at the time of launch, and much more once HYPE’s price exploded) means the validator set might be somewhat limited to well-capitalised and savvy operators. Still, the Hyperliquid Foundation and community can encourage decentralisation by perhaps lowering staking requirements or providing guides and incentives for more validators around the world. Notably, Hyperliquid’s chain state and matching engine are deterministic, so having more independent validators increases trust that no single party can manipulate orders or censor transactions.

One sign of decentralisation progress: the foundation did not keep special control keys or multisigs for upgrades; instead, upgrades and certain actions (like using the Assistance Fund in emergencies) require validator consensus or governance votes. That means changes to core protocol parameters should ultimately go through community-driven processes.

Hyperliquid Improvement Proposals (HIPs)

To involve the community in decision-making, Hyperliquid employs a governance framework similar to Ethereum’s EIPs or Uniswap’s proposals, aptly named Hyperliquid Improvement Proposals (HIPs). These can range from technical upgrades to economic changes or new feature introductions. Some of the key HIPs so far:

HIP-1: Native Token Standard. This proposal defines how new tokens (spot assets) can be created on Hyperliquid, setting the stage for permissionless listings. It essentially established a token standard on Hyperliquid L1 (comparable to ERC-20 on Ethereum), which all spot trading assets follow. This was foundational for later allowing community projects to launch tokens on Hyperliquid and have them trade on the order book.

HIP-2: Hyperliquidity. As discussed, HIP-2 introduced the Hyperliquidity automated market-making strategy for spot markets. This was likely proposed by the core team to ensure new token markets have baseline liquidity. It’s a fully on-chain algorithm (part of block execution) that doesn’t require any centralised control, aligning with decentralisation—once implemented, it just runs as code, securing the order books for certain assets. The genesis token distribution even allocated 120k HYPE to this initiative, presumably to seed initial liquidity or reward that strategy.

HIP-3: Builder-Deployed Perpetuals. This HIP enabled external developers to permissionlessly create perpetual futures markets on Hyperliquid. It’s a big step toward decentralising the exchange’s growth—Hyperliquid’s team doesn’t solely decide what markets to list; anyone can deploy a market (provided they follow certain conditions like asset standards and perhaps staking some HYPE as collateral). HIP-3 essentially opened Hyperliquid to a wider array of trading products, limited only by community creativity. For example, we have seen markets for new tokens and even index products (“Hyperps”) created via this route.

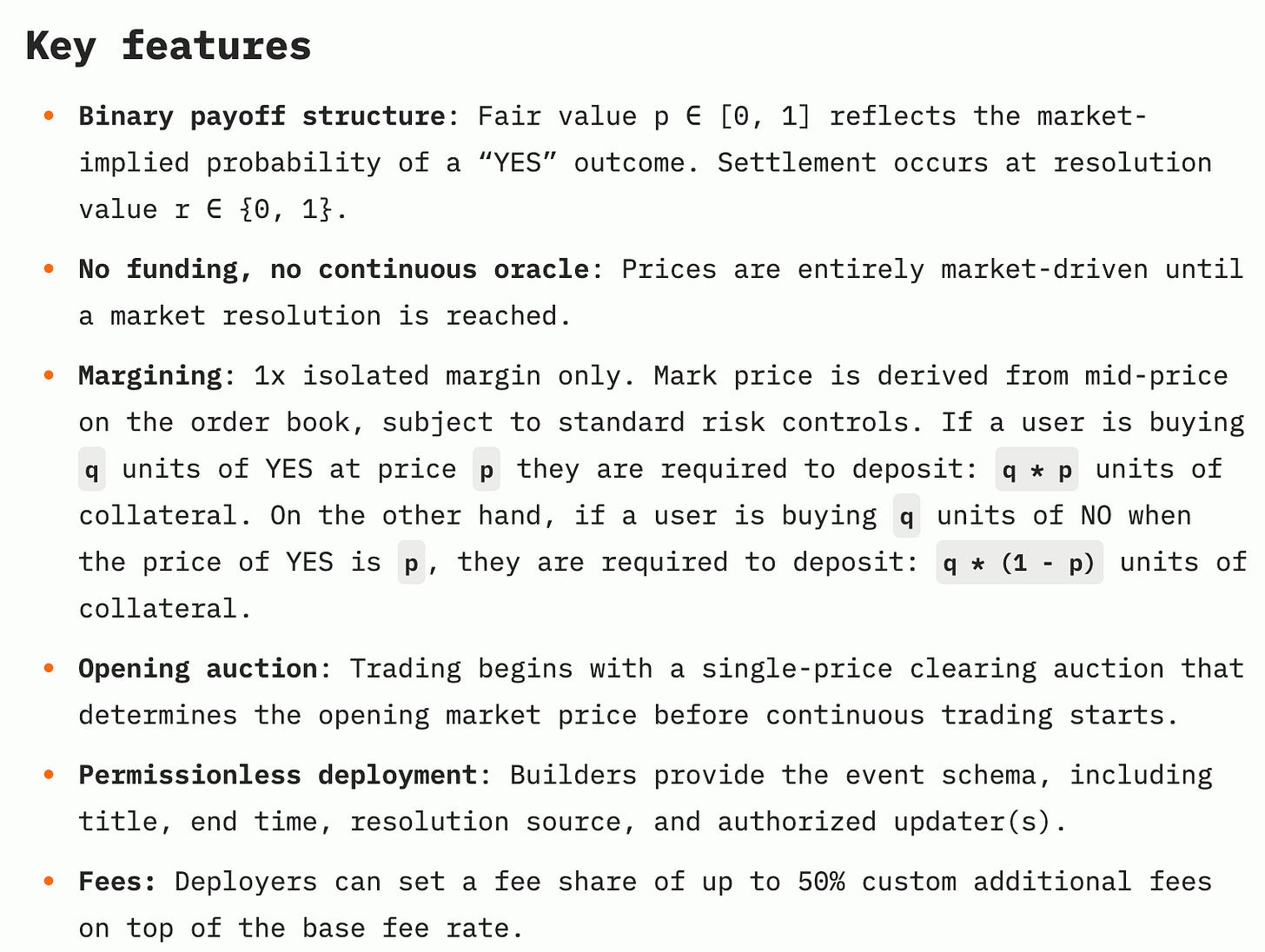

HIP-4: Event Perpetuals (Prediction Markets). This is a recent proposal (Sept 2025) that showcases how community and even external entities are now driving innovation on Hyperliquid. HIP-4, co-authored by members of the community and a head of crypto at Kalshi, proposes “Event Perpetuals”—essentially turning Hyperliquid into a venue for prediction markets like sports bets, election outcomes, etc., using a novel perpetual contract design. The motivation was that traditional perps (with continuous funding and oracle price feeds) aren’t well-suited for binary events. HIP-4 suggests removing oracles and funding for these special markets; instead, they would use trading activity to price the binary outcome, and settle at 0 or 1 based on the event result. An auction mechanism would determine a fair opening price over a 15-minute window before trading commences, addressing the challenge of low-liquidity price discovery.

HIP-4 To ensure only serious markets are created, market creators would need to stake 1,000,000 HYPE (a hefty sum, ~$40–50M at current prices) and can charge an extra fee on their markets as compensation. This proposal, if implemented, could unlock entirely new use cases (on-chain betting) on Hyperliquid’s infrastructure, leveraging its performance for quick settlement of, say, 15-minute event auctions. The fact that a Kalshi executive and other community members drove HIP-4 indicates Hyperliquid is becoming an ecosystem, not just a product run by one team. (It’s also poetic, given Jeff Yan’s first crypto project attempt was a prediction market—now the concept is coming full circle via Hyperliquid).

Other HIPs and Discussions: Beyond the numbered proposals, there have been governance discussions around referral programs (e.g., a proposal to share staking referral rewards), fee structure changes (like the decision to cut trading fees by 80% ahead of token launch, which was executed in late 2024 to drive volume), and of course the HYPE supply reduction proposal by DBA/Hasu (which might be formalized as a HIP vote).

Gradual Decentralisation of Operations

In the early days, the Hyperliquid team likely ran critical infrastructure (order matching code, upgrade deployments) in a somewhat centralised fashion for efficiency. But as the platform matures, they have been open-sourcing more components and involving the community in operations. For instance:

Open Sourcing: Key parts like the Hyperliquid node software and SDKs are available for anyone to run, and developers are building analytics and tools around it. (Hyperliquid’s block explorer and stat pages are community-driven in some cases, e.g., DefiLlama integrating Hyperliquid data.)

Foundation and Builder Ecosystem: The Hyperliquid Foundation plays a role akin to other L1 foundations—supporting development and ecosystem growth with its treasury (6% of supply). But the foundation doesn’t overtly dominate; they have empowered independent builders. For example, Phantom (a popular Solana wallet) integrating Hyperliquid’s trading directly was a huge win that came from outside—and it led to a notable bump in users and volume in mid-2025. The foundation likely facilitated such partnerships, but the point is, Hyperliquid isn’t trying to build every ancillary service itself. It relies on an ecosystem of wallets, interfaces, and developers adding value on top.

Community Support Programs: With grants and incentives, Hyperliquid is encouraging third-party projects—whether it’s someone creating a better analytics dashboard, or launching a new financial product on HyperEVM that uses Hyperliquid’s liquidity. This “ecosystem-based approach” means Hyperliquid focuses on the core protocol while others extend it. It contrasts with, say, a centralised exchange that tries to lock users into its own app for every feature. Hyperliquid’s approach is more akin to a protocol that anyone can tap into. This is evidenced by the Builder Codes program (monetisation for external apps) and the emphasis on composability.

Decentralised Front-Ends: One area to watch is whether Hyperliquid will decentralise its front-end interface. Currently, many users trade via the official Hyperliquid web app (which, while non-custodial, is still a hosted website). To be fully censorship-resistant, the community could host alternative front-ends or IPFS-hosted UIs. Given the permissionless API, this is feasible—we might see community-driven front-ends, especially for specialised markets (e.g., a front-end tailored for prediction markets if HIP-4 passes).

Challenges: Despite all these efforts, decentralisation is a journey. Hyperliquid does face some centralisation pain points:

Validator Diversity: Ensuring a wide distribution of validators geographically and by ownership is crucial. If too few entities control validation, the network could be attacked or censored. The high hardware requirements and staking amount could concentrate validators among wealthy insiders or funds. Over time, the community might consider methods to broaden this (lowering stake requirements, incentivising smaller validators, etc.).

Governance Participation: With only ~94k token holders initially (and likely a smaller subset holding significant amounts), governance could be dominated by a few large holders (possibly whales who got big airdrops or the core team’s votes once their tokens unlock). The team’s tokens are locked until the end of 2025, effectively giving the community a year of governance without team voting power. But come 2026, one must hope the team uses its power responsibly or continues to defer to community sentiment. The silver lining: no VCs means there isn’t an overbearing investor bloc—the team and users’ interests are more aligned than in many projects.

Transparency and Code Audits: The Hyperliquid codebase, especially the consensus and matching engine, is complex. The team has had it audited (they mention multiple audits for bridges, etc.), but ongoing transparency is key. Open-sourcing everything and allowing community devs to contribute will strengthen trust. Given Hyperliquid’s volumes, any bug could be very costly, so the community has to stay vigilant through bug bounties and reviews.

Overall, Hyperliquid has so far threaded the needle well: it launched as a somewhat centralised project (out of necessity to build it) but quickly gave ownership to users and is now incrementally giving control to the community. This trajectory mirrors other successful projects (like how Uniswap retroactively airdropped tokens and instituted governance). The major difference is that Hyperliquid operates an entire L1 order-book exchange, which historically was thought too performance-sensitive to decentralise. Hyperliquid is proving that notion wrong—decentralisation and high performance can coexist, though it requires ingenuity.

Next, let’s examine how Hyperliquid’s rise has impacted the broader DEX landscape and what competition is brewing, as well as how the “Hyperliquid model” might influence future crypto startups.

The New Landscape

Hyperliquid’s explosive success essentially kicked off a new arms race in DeFi: the race to build high-performance, on-chain order book exchanges. In 2021–2022, decentralised trading was dominated by AMMs (Uniswap, PancakeSwap) and a few niche order book venues. By late 2024 and into 2025, Hyperliquid changed the game, proving that a DEX could achieve CEX-like performance. Competitors and new entrants took notice. Let’s survey the landscape post-Hyperliquid:

Hyperliquid’s Early Dominance

For much of 2024 and early 2025, Hyperliquid was the undisputed leader in decentralised derivatives. By mid-2025, it commanded around 70% of the market share in perpetual DEX trading. Daily volumes of $10B+ on Hyperliquid became routine, dwarfing other on-chain competitors. Hyperliquid’s combination of deep liquidity, many trading pairs, and a strong reputation made it the go-to venue for serious traders seeking a DeFi alternative to the likes of Binance or Bybit.

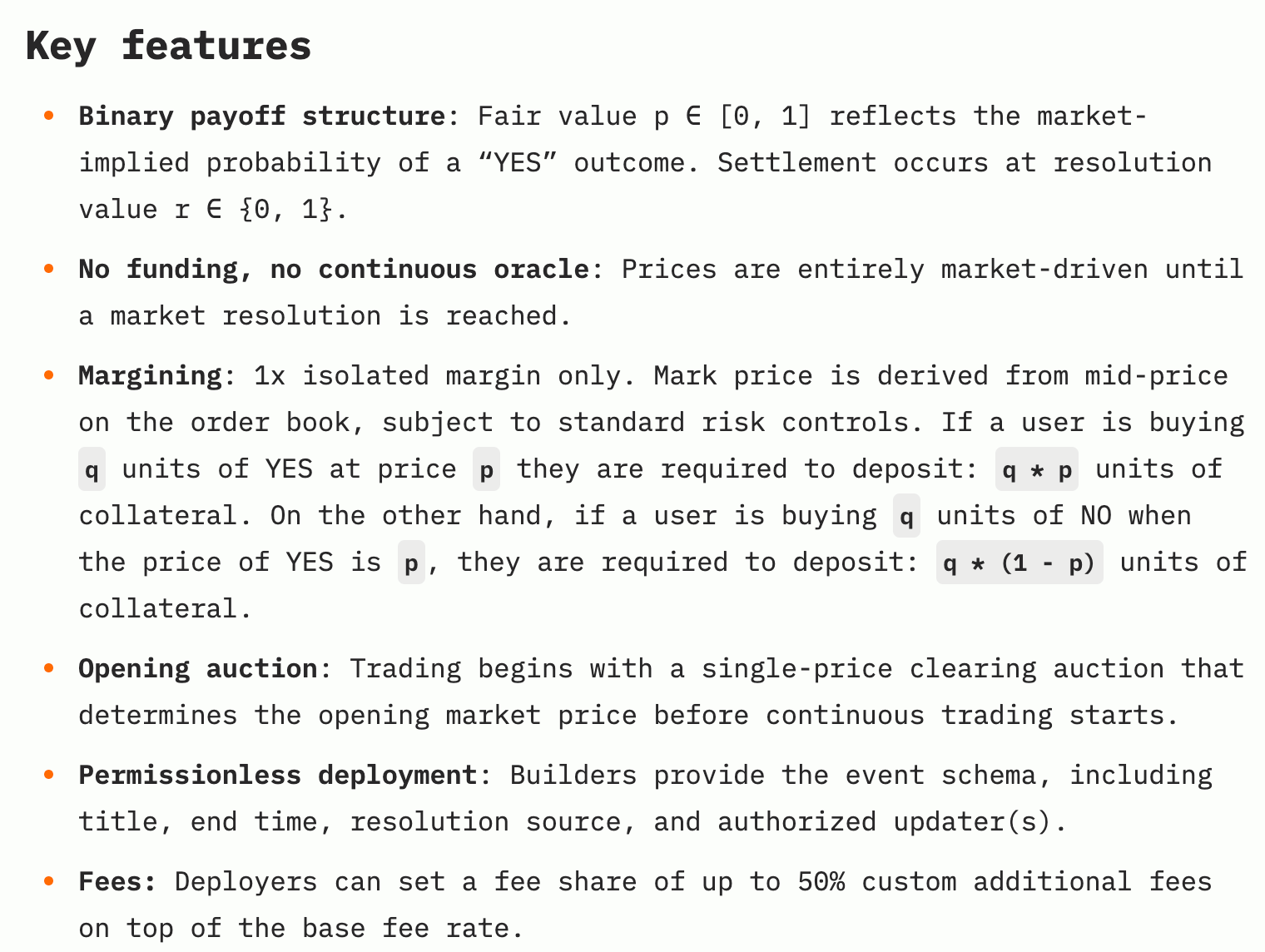

Not only did it lead in volume, but Hyperliquid also built up significant open interest (OI)—essentially the total value of active positions. Even as competition later heated up, by October 2025, Hyperliquid’s OI remained >4× larger than its nearest competitor’s. This indicates that traders still trust Hyperliquid the most for keeping large positions over time, a sign of its credibility and robust risk management.

The Rise of Aster and Lighter

Around mid-to-late 2025, two notable rivals emerged, leading to what some called the “Perpetual DEX Wars”:

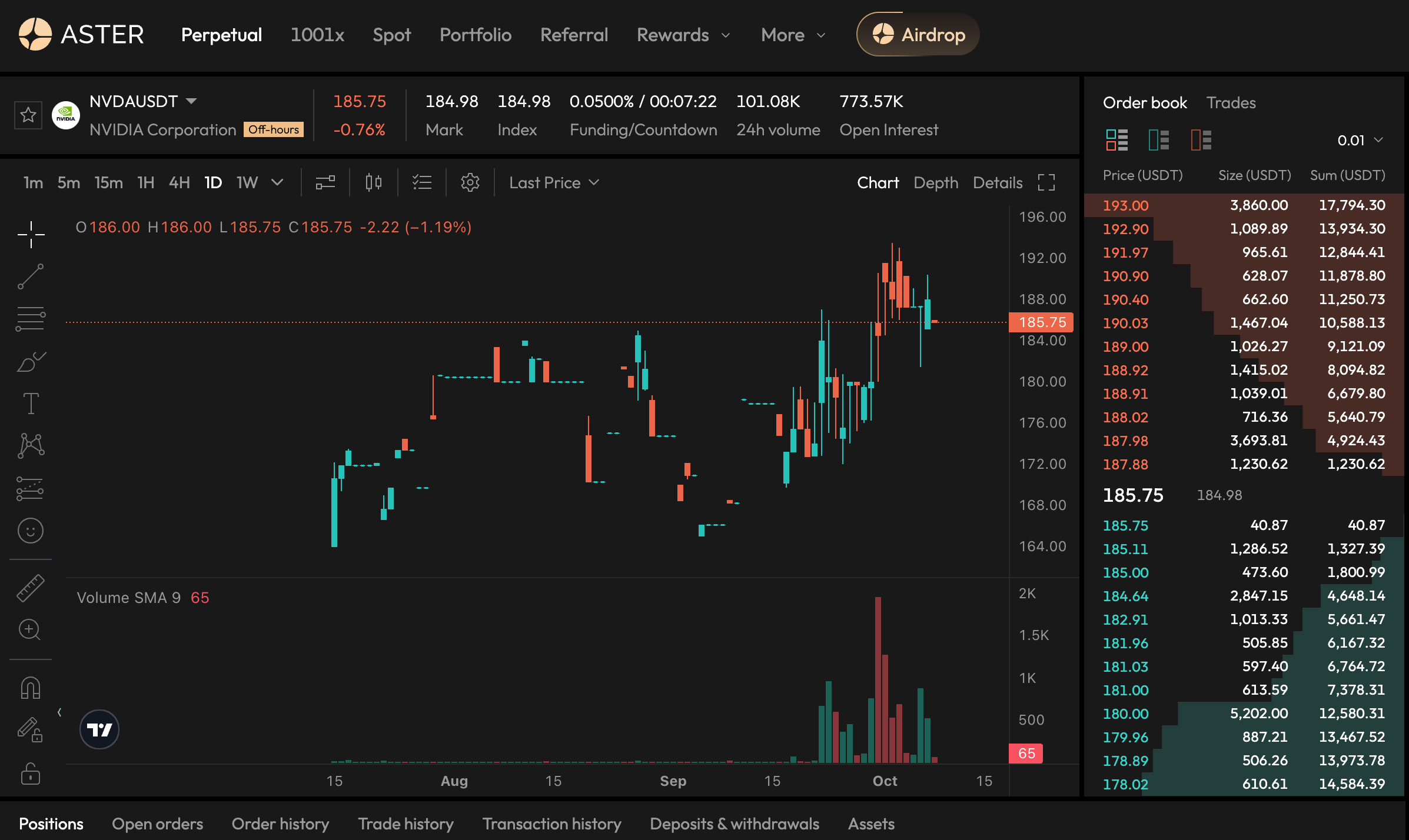

Aster: Launched in 2025, Aster took a different approach by going multi-chain from the start. It deployed on multiple networks—Ethereum, BNB Chain, Solana, and Arbitrum—aiming to capture users across ecosystems. Aster offers two modes: a Simple Mode using an automated liquidity pool (like a GMX-style AMM with up to 1001× leverage, via an ALP pool) and a Pro Mode with a CLOB interface for advanced traders. This hybrid approach is interesting: Aster tries to cater to both AMM-style users and order book users.

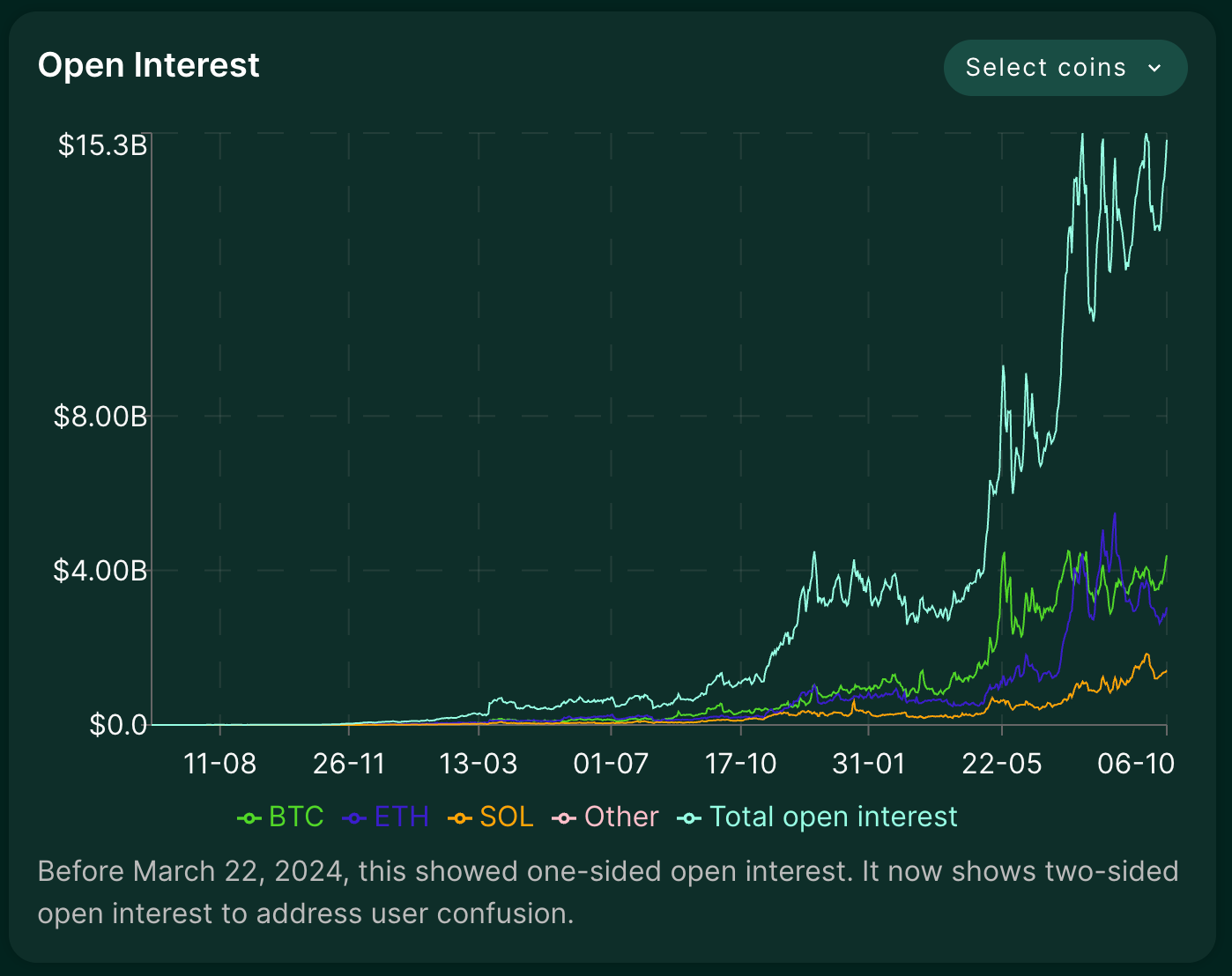

Trading NVIDIA on Aster Aster also innovated with stock perpetuals—allowing crypto traders to speculate on stocks like NVIDIA, Apple and Tesla with crypto collateral. This bridging of traditional equities into DeFi is something Hyperliquid hasn’t done (Hyperliquid focuses mainly on crypto assets), and it certainly attracted attention. By October 2025, Aster executed an aggressive liquidity mining campaign (with a points-based trading reward system) that caused its volumes to skyrocket from ~$1B/day to $70B/day within a week. This gave Aster nearly 70% market share by raw volume in early October 2025, temporarily eclipsing Hyperliquid. However, on-chain sleuths suspect much of Aster’s volume was incentivised or even wash-traded to farm rewards—its volume/TVL ratio was an absurd >70, far above normal, hinting the growth wasn’t purely organic. Still, Aster has positioned itself as a serious contender, backed by endorsements from notable figures like Binance’s CZ. Aster shows that the competition is not standing still; features like MEV-protected trading, multi-chain accessibility, and unique markets (stock perps) are being tried to one-up Hyperliquid.

Lighter: Another entrant is Lighter, which differentiates itself through zero-knowledge proof technology. Lighter runs on a custom zkRollup on Arbitrum, where every trade and update is validated by zero-knowledge proofs. The focus here is on provable fairness and security—a fully verifiable DEX where users don’t have to trust even the validators, because cryptographic proofs ensure the rules were followed. Lighter also launched a bold zero-fee model for retail traders (likely monetising elsewhere or planning to later). By October 2025, while still in invite-only beta, Lighter was already processing ~$8B daily volume.

Trading ASTER Token on Lighter Its emphasis is not on outpacing Hyperliquid’s speed (indeed, proofs add some latency and cost), but on offering maximum trustlessness—something that could attract users who prioritise security and fairness (for instance, proofs that no MEV or order manipulation occurred). Lighter’s approach underscores a segment of competition focusing on cryptographic guarantees as the next frontier.

dYdX and Others: It’s worth mentioning dYdX, the prior leader in decentralised perps (which operated an order book on an Ethereum L2, StarkEx). dYdX’s volumes stagnated in 2023–2024, and it decided to migrate to its own Cosmos-based chain (dYdX v4). That launch has taken time, and Hyperliquid essentially swooped in during the interim and captured the market. It remains to be seen if dYdX v4 can reclaim users—it will have to compete directly with Hyperliquid on performance and incentives, which won’t be easy without a similar community distribution. Other projects like GMX (an AMM perps model) continued to do well in their niche (simple UI, smaller tokens), but for high-volume trading, the narrative shifted to Hyperliquid and clones of its model.

The competitive dynamics now resemble a three-way race (Hyperliquid, Aster, Lighter). Each offers distinct trade-offs: Hyperliquid = pure performance and deep liquidity (the “CEX experience on-chain” pioneer), Aster = cross-chain convenience and novel assets but possibly incentive-driven volume, Lighter = max decentralisation/trust with innovative tech but early-stage. It’s a healthy competition, as each is pushing the others to improve.

For example, Aster’s liquidity mining surge likely spurred Hyperliquid’s community to consider how to respond (though Hyperliquid has refrained from short-term incentive wars so far, focusing on organic growth and its buyback model). Lighter’s zk-proof model presents a benchmark for Hyperliquid in terms of verifiability; one could envision Hyperliquid adopting similar techniques or even deploying rollups on top of it in the future.

One clear outcome: order book DEXs are now a major category in DeFi, whereas two years ago, many assumed only AMMs would survive on-chain due to complexity. Hyperliquid opened the door, and now others are walking through.

Hyperliquid’s Lasting Influence on DeFi Projects

Beyond direct competitors, Hyperliquid’s success may have a broader influence on how crypto projects are built and launched:

Lean, Product-Focused Teams: Hyperliquid demonstrated that a tiny team can deliver an industry-leading product. This challenges the paradigm of giant developer teams or heavily funded projects as a requirement for success. Future founders may emulate this “minimal headcount, maximal output” approach, concentrating talent and avoiding the coordination issues of large teams. It also helps that with small teams, token distribution can more heavily favour users (since there aren’t dozens of insiders to allocate to).

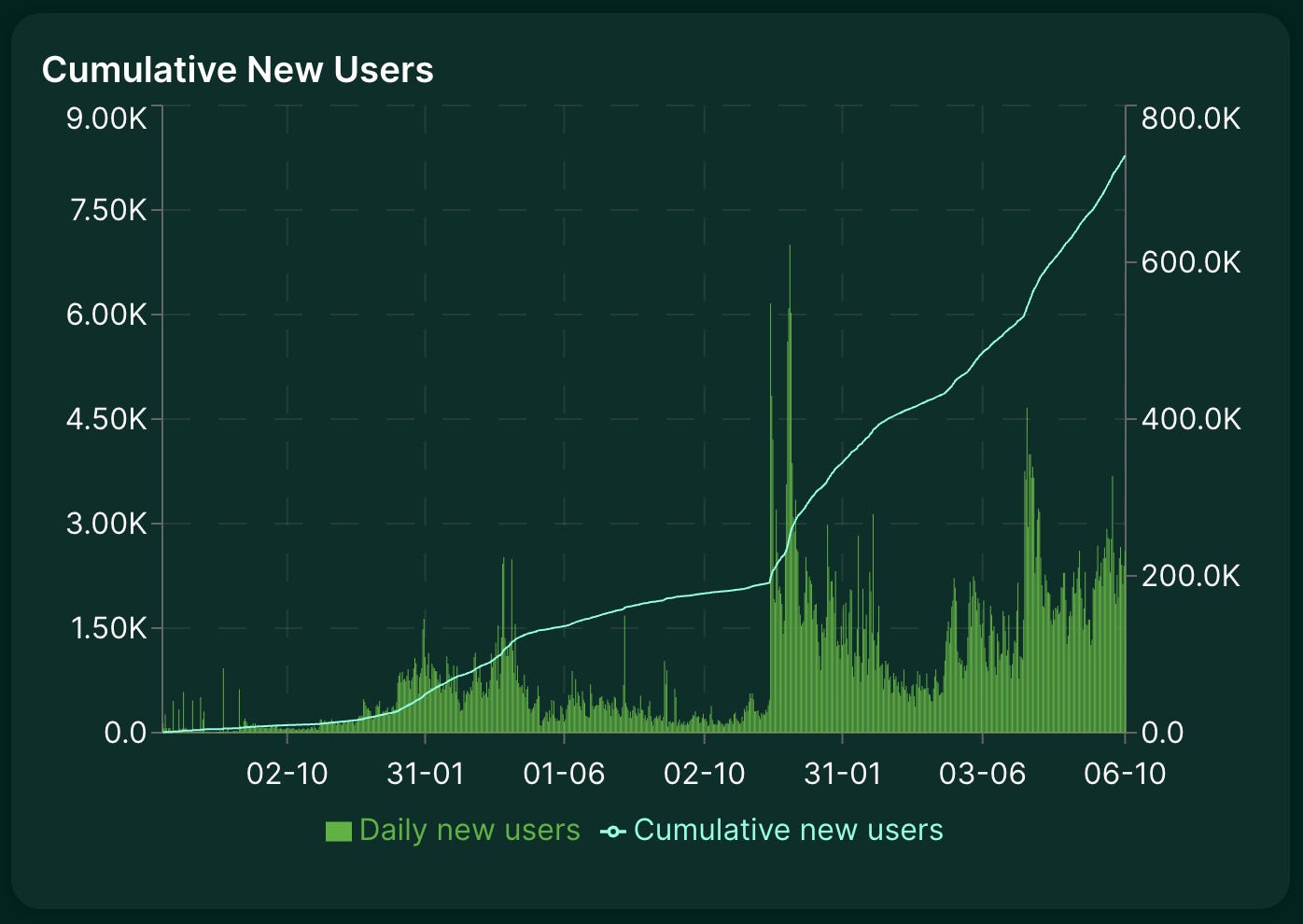

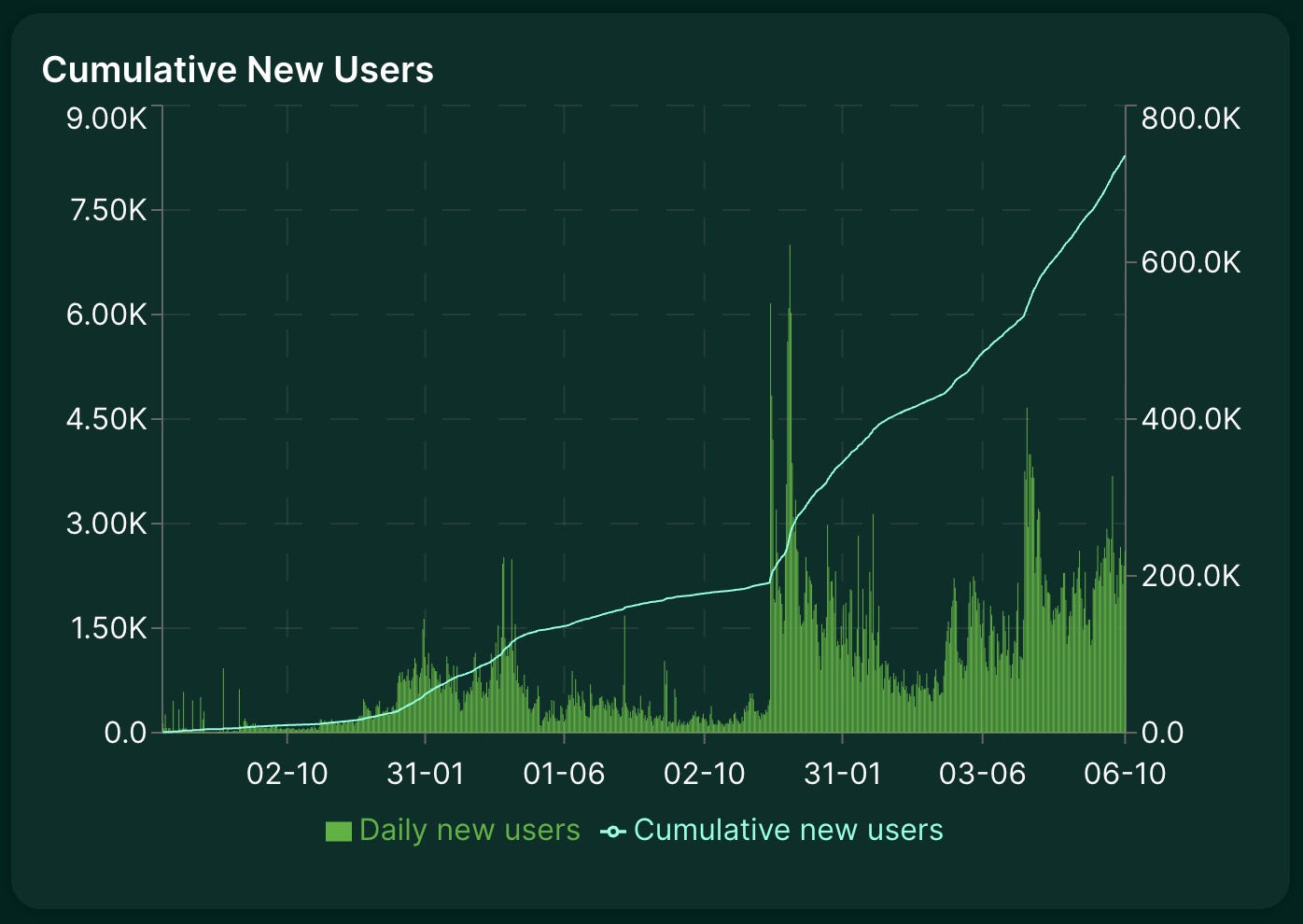

Cumulative new users trading on Hyperliquid over time Community Ownership as GTM: Hyperliquid’s user-centric token launch (massive airdrop) was risky—giving away value without direct monetary return. But it paid off in loyalty, WOM marketing, and network effects. Projects in the future might adopt similar strategies: foregoing or limiting VC funding, engaging users early (via testnet points or loyalty programs), and then doing a big community distribution. We have already seen projects like Arbitrum and Optimism in 2023 use airdrops to decentralise. Hyperliquid took it to another level in terms of scale relative to its market cap. If those users stick around (and by most metrics they have—Hyperliquid’s active user count has been strong, then it’s a strategy that others will study closely.

App-Specific Chains and Custom Infrastructure: There is renewed interest in appchains. Hyperliquid is a prime example of an appchain that outperformed on a specific use case. Now, other DeFi sectors might consider this route. The Cosmos ecosystem and Polygon Supernets are facilitating such app-specific chains. Hyperliquid chose to roll its own chain (with EVM compatibility for flexibility)—a non-trivial path, but ultimately allowed unmatched optimisation. It sets a precedent: if you need extreme performance, build vertically (your own chain) rather than relying on slow general layers. The upcoming dYdX chain and even things like Sei Network (a general-purpose trading-focused L1) are part of this trend that Hyperliquid now dominates.

Blurred Lines with TradFi: Hyperliquid and its peers inch DeFi closer to traditional finance’s capabilities. This could attract institutional participation in these decentralised venues. For instance, by Q3 2025, institutional custodians like BitGo added support for Hyperliquid’s network, making it easier for funds to hold and trade HYPE or use Hyperliquid through custodial services. As DeFi platforms meet TradFi performance standards, we might see more crossover—maybe market makers who traditionally operate on NASDAQ or CME will provide liquidity on Hyperliquid; perhaps professional traders will prefer Hyperliquid for certain assets due to 24/7 global access and self-custody of funds.

Security and Resilience as Selling Points: Hyperliquid’s handling of incidents (like reimbursing users after an outage) and its non-custodial nature could set a higher bar for user protection. If a decentralised platform can be as user-responsive as a centralised one, users will naturally gravitate to the one where they also hold their keys. Competitors and new projects will need to match this level of user assurance—whether through insurance funds, rigorous audits, or governance that can react quickly to issues.

In essence, Hyperliquid altered the trajectory of DeFi. The sector is no longer content with slow AMMs or clunky UX in the name of decentralisation. Users want the best of both worlds: speed and trustlessness. Hyperliquid provided a template for achieving that. And by proving the viability of community-owned, high-performance exchanges, it likely changed investor and developer calculations. Why build a centralised exchange startup (with all its regulatory and custodial headaches) when you could build the next Hyperliquid? Why give the majority equity to VCs if a community token can provide both funding (if some tokens are sold) and a built-in user base?

That’s not to say everything is perfect or that CEXes are obsolete—centralised platforms still have larger volumes overall and mainstream user bases. But the gap is closing. And it’s hard to disagree when daily volumes on these DEXs are now in the same ballpark as major CEXs.

The Road Ahead

As we look to the future, several threads will determine Hyperliquid’s trajectory and its broader impact on DeFi:

1. Maintaining the Edge in Technology: Hyperliquid will need to keep innovating to stay ahead. This could involve further optimising HyperBFT (perhaps incorporating newer consensus research to push latency even lower) or scaling throughput as user numbers grow. The chain might explore layer-2 solutions itself—for instance, spawning rollups that settle on Hyperliquid L1 to partition load, similar to how some CEXs have multiple matching engines. Given competitors like Lighter are leveraging zk-proofs, Hyperliquid might integrate more cryptographic verifiability into its model (maybe optional zk-proof verification for trades, to combine performance with provability). Staying at the cutting edge will ensure Hyperliquid retains the title of fastest, most advanced DEX.

2. Decentralisation Milestones: By late 2025, the big event will be the unlock of core contributors’ tokens (23.8% supply) after the 1-year cliff. How the team handles this will be closely watched. They have vested interest (pun intended) in not spooking the market—likely the team will be transparent and possibly even self-impose further lock-ups to signal commitment. If some portion is sold, it could be done via OTC deals or slowly to minimise impact. Successfully navigating this will increase confidence in Hyperliquid’s decentralisation (the team making decisions alongside, not above, the community).

Meanwhile, governance participation should ramp up. We might see HYPE staking for voting (similar to how Curve uses vote-locking), or other measures to boost community voice. If HIP-4 (event perps) passes and is implemented, it will be a flagship example of community-driven expansion of the product. The outcome of the 45% supply burn vote (if it proceeds) will also be pivotal: a yes vote would demonstrate decisive action to favour token holders; a no vote might indicate preference for keeping rewards for future growth. Either way, it sets a precedent for token governance in a major protocol.

3. Ecosystem Expansion: With HyperEVM live, the stage is set for an ecosystem of apps around Hyperliquid. We already saw a top Solana wallet (Phantom) integrate directly. In the future, perhaps MetaMask or other multi-chain wallets will integrate Hyperliquid trading (especially if liquidity remains superior). We may see structured products (like structured vaults) built on Hyperliquid—e.g., vaults that algorithmically trade on Hyperliquid or do copy-trading. Also, lending protocols on HyperEVM could use Hyperliquid positions as collateral (imagine taking a loan against a Hyperliquid perp position, which would basically be a cross-margin across DeFi apps).

Hyperliquid’s foundation has resources (6% treasury plus any fees they might retain) to invest in these ecosystem projects or run hackathons. If the community grant program (0.3% of supply) is put to use, we might hear about grant recipients building novel use cases.

4. Crossing into Real-World Assets: One avenue Hyperliquid hasn’t publicly pursued yet is real-world asset trading. Aster’s stock perps hinted at demand for trading non-crypto markets on DeFi rails. It wouldn’t be surprising if Hyperliquid eventually lists tokenised versions of stock indices, commodities, or Forex pairs—provided there’s a reliable oracle or a way to do so compliantly. The barrier is regulatory (and Oracle trust). But partnerships with firms like Kalshi (as in HIP-4) suggest a path to quasi-regulated prediction markets or event markets, which are a cousin of real-world assets. If Hyperliquid could allow, say, S&P 500 or gold price exposure on-chain, it would open a huge new user base and differentiate from purely crypto-focused rivals.

5. Navigating Regulation: Speaking of regulation, as Hyperliquid grows, it will catch more eyes in the regulatory sphere. Decentralised derivatives are already a grey area. Hyperliquid’s advantage is that it’s not operated by a company offering services; it’s a protocol. However, regulators might target front-ends or classify the DAO/foundation as an operator. How Hyperliquid responds—possibly geo-blocking the official front-end in certain jurisdictions, or encouraging users to access via alternate means—will be delicate. In the long run, truly decentralised control (no central party to pressure) is the best defence. If Hyperliquid sufficiently decentralises governance and infrastructure, it can claim to be akin to Bitcoin or Ethereum—a public network that can’t be easily shut down. The challenge is ensuring the UI layer is also censorship-resistant (perhaps through IPFS or community-run interfaces). We might see more messaging from Hyperliquid on compliance (they have been relatively quiet on that front publicly). Interestingly, Hyperliquid did not force KYC or region locks from the start, likely because the protocol-level approach makes that difficult. But as a precaution, many DeFi projects have eventually added front-end warnings or soft blocks for US IPs, etc. The community might have to grapple with this to protect the protocol from unwanted enforcement actions.

6. Continued Market Leadership vs. Competitors: Hyperliquid will no doubt respond to Aster, Lighter, and the next wave of challengers. If Aster’s volume is largely mercenary (farming-driven), Hyperliquid might bet on those traders returning or those incentives dying down. But if Aster’s cross-chain strategy proves popular, Hyperliquid could consider its own multi-chain expansion. One intriguing idea is Hyperliquid, perhaps launching “satellite” deployments on other chains that tap into Hyperliquid’s liquidity. For example, a rollup on Ethereum that settles to Hyperliquid’s chain or a Uniswap-style interface on other L1s that routes to Hyperliquid could capture users in those ecosystems without making them bridge manually.

Feature-wise, if competitors add something attractive (e.g., Aster’s hidden orders to combat MEV, or yield-bearing collateral for margin trading), Hyperliquid can consider similar or better implementations. It already has a lot—advanced order types, etc.—but DeFi moves quickly, and innovation is often open-source and composable.

7. Inspiring the Next Wave of dApps: Perhaps one of Hyperliquid’s most important legacies will be the teams it inspires. The notion that a startup can forego VCs, launch with a product-first approach, and then do a big community token is powerful. It offers a path for bootstrapping communities without the regulatory complexity of equity or token sales (airdrops, while not without questions, have been more tolerated so far).

We might also see existing projects adopt Hyperliquid’s tokenomics elements—for instance, increasing fee buyback allocations. Arbitrum, for instance, launched with a token but no explicit fee burn mechanism, which some in its community have discussed later. Hyperliquid showed a rather extreme case of revenue return to token holders (via buybacks), which could influence governance decisions in other DAOs: token holders everywhere like the idea of value accrual.

8. Potential Collaboration with Traditional Finance: In a forward-looking scenario, Hyperliquid’s tech could even attract TradFi exchanges or institutions. We could imagine a future where a major exchange or brokerage partners with Hyperliquid to offer on-chain trading to their clients. If Hyperliquid’s volumes and liquidity remain high, being connected to it could be a selling point (the way some fintech apps integrate with Coinbase or Uniswap for crypto liquidity). Hyperliquid might not directly chase this, but the openness of the protocol means others can leverage it. We already saw BitGo enabling HYPE custody. If down the line, say, a regulated fund wants exposure to Hyperliquid’s yields or fees, they might acquire HYPE or run validators.

Finally, consider the bigger picture of DeFi innovation: Hyperliquid’s success indicates that decentralisation need not come at the cost of performance. It also reaffirms a core DeFi principle—users become stakeholders. In Hyperliquid’s case, users literally became significant stakeholders via the token distribution. That creates an army of advocates. If future dApps adopt that model, we could see a renaissance of user-owned finance applications outcompeting not just their decentralised predecessors, but also putting pressure on traditional incumbents with superior alignment and often lower fees (since no need to extract profit when you give it back to token holders).

In closing, Hyperliquid’s journey from a stealth project by a handful of cracked builders to a multi-billion-dollar, community-driven protocol is a case study in what’s possible in Web3. It combined the best of TradFi engineering with the ethos of crypto. As a result, it created a new standard for what a decentralised exchange can achieve. The narrative arc—from the FTX collapse lighting a spark in a trader’s mind, to a small team building a rocketship blockchain in a garage, to distributing that rocket’s ownership to its earliest riders, and now watching it soar—is the stuff of tech legends.

Whether Hyperliquid itself remains at the very top in the years to come, it has already altered the course of DeFi’s evolution. Future teams will cite Hyperliquid’s example when choosing to stay lean and community-focused. Future dApps will aim to be as seamless and fast. And the concept of “community as shareholders” that Hyperliquid epitomised, following the footsteps of stalwarts like Uniswap, Arbitrum, Optimism, etc, will likely become the norm. For anyone involved in crypto—newbie or veteran—Hyperliquid’s story offers both inspiration and a wealth of lessons, from technical design to token economics to community building. It’s a reminder that sometimes, the quietest players build the biggest things. Hyperliquid started quietly, but today it stands loud and clear as a pillar of decentralised finance, and its ripple effects are only beginning to be felt.

I am Jeswin. Former BD and Marketing Lead for a major protocol. I am in between jobs right now, and getting back to my main thing, Research and Writing. You can find me on X or Telegram. Looking forward to hearing your feedback and questions.